The main changes contained in the Pfandbrief Act Amendment 2021

Dr. Otmar Stöcker

Association of German Pfandbrief Banks

05.2021

In mid-April of this year, the German Bundestag passed the Covered Bonds Directive Implementation Act (CBD-Umsetzungsgesetz, CBDUmsG). This legislative package, which is aimed primarily at implementing the EU’s Covered Bonds Directive (CBD) and at making adjustments to reflect the changes to article 129 of the Capital Requirements Regulation (CRR), contains an extensive amendment of the German Pfandbrief Act (Pfandbriefgesetz, PfandBG).

EU harmonisation of covered bonds

The changes to the law provide for adjustments to the PfandBG in order to reflect EU covered bond harmonisation measures. In addition, the draft ensures that all Mortgage Pfandbriefe, Public Pfandbriefe and Ship Pfandbriefe will continue to satisfy the qualification preconditions of amended article 129 CRR and can thus benefit from the associated privileges granted.

Entry into force

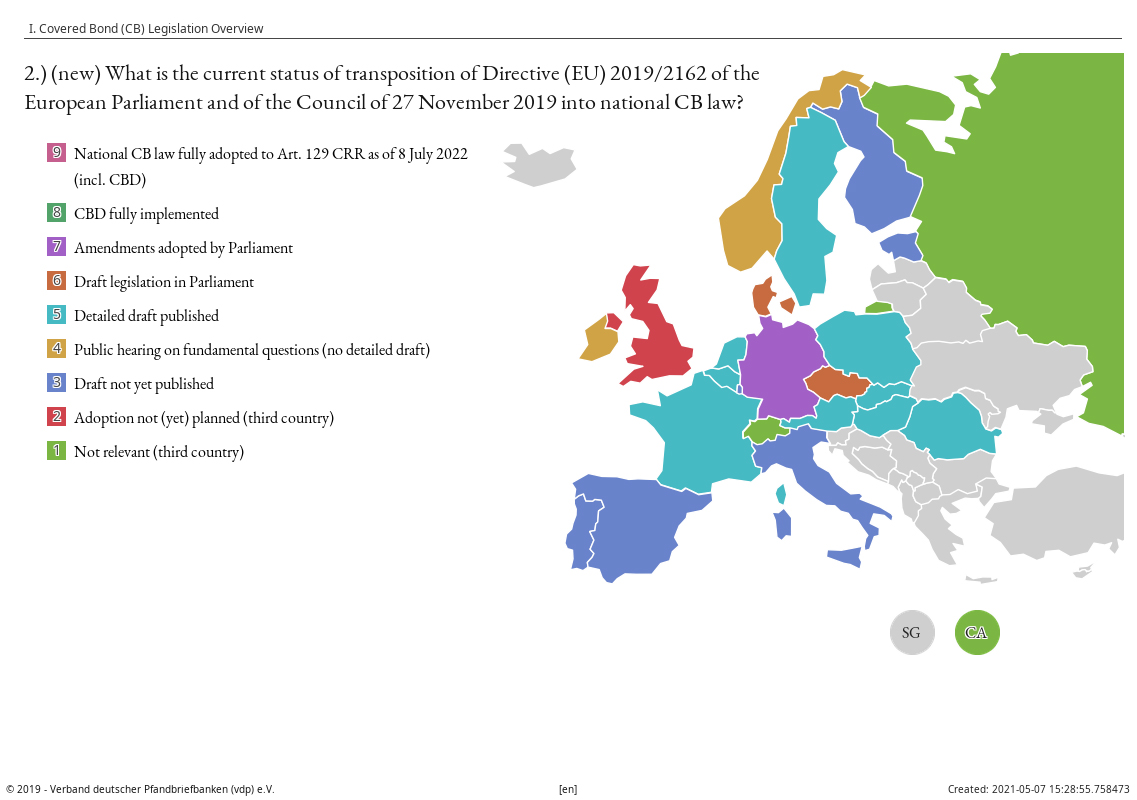

On 15 April 2021, the German Bundestag passed the bill with the amendments recommended by its Finance Committee.1 The second reading in the Bundesrat took place 7 May 2021. Germany therefore is the first country to complete the parliamentary procedure for implementation of the CBD.

The entry into force of article 1 CBDUmsG, including, in particular, the provisions on building insurance and on maturity extension on 1 July 2021 – i.e., a few days before expiry of the deadline to implement the CBD on 8 July 2021 – is therefore assured. Accordingly, article 2 CBDUmsG, including provisions on implementing the CBD, will enter into force on 8 July 2022, the same date from which the amended article 129 CRR will apply with immediate effect.

Source: Roundtable Covered Bond Legislation

A detailed look at the adjustments

Below, the main changes made to the PfandBG by the 2021 Amendment broken down into the relevant paragraphs are introduced and discussed:

-

Section 4 PfandBG – Calculation of coverage, overcollateralisation

In order to implement article 15 (3) 2 CBD, the previous net present value of statutory overcollateralisation of 2 % has been converted to a lump sum for the costs of winding-down.

Moreover, to adapt the PfandBG to article 129 (3a) 3 CRR, an additional “nominal statutory overcollateralisation” is introduced, the nominal value of which will be 2 % for Mortgage and Public Pfandbriefe; 5 % will be required for Ship Pfandbriefe and for Aircraft Pfandbriefe.2

-

Section 4 (1a) PfandBG – Liquidity buffer

The provisions regarding the liquidity buffer are being adjusted to reflect article 16 CBD. In particular, in future, the only assets that can be used for the liquidity buffer are those meeting the requirements of the LCR Regulation, as well as short-term risk exposures to credit institutions with adequate credit quality.3

-

Section 4b PfandBG – Derivatives eligible for inclusion in cover pool

Provisions on derivative transactions eligible for inclusion in cover assets that were previously contained in various provisions of the PfandBG have been combined in the new section 4b PfandBG.

-

Section 8 (4) sentence 2 PfandBG – Cover pool monitor’s approval for deletions

For cover registers that are kept electronically, in future it will be possible to obtain the cover pool monitor’s approval to delete cover assets in electronic form if the statement is adequately documented and authenticated. Documentation and procedural requirements will be defined in the upcoming revision of the Cover Register Statutory Order. This is intended to facilitate the issuance of electronic approvals and, by extension, to simplify electronic management of the register.

-

Section 15 PfandBG – Building insurance

For building insurance, maximum annual compensation is expressly permitted for the owner’s group insurance, for the Pfandbrief bank’s insurance against default and for the insurance of an individual building by the owner, but in the latter case excluding fire insurance.

The Pfandbrief bank’s contingency insurance is expressly no longer required to insure for more than the loss of the current value for which the Pfandbrief bank would receive payments from the owner’s building insurance.

-

Section 28 PfandBG – Transparency

The provisions on transparency are being expanded, in particular to include disclosures about statutory, contractual and voluntary overcollateralisation and on the preconditions for a maturity extension, the associated powers of the cover pool administrator and the effects of such a maturity extension on the maturity structure of Pfandbriefe.

-

Section 30 (2a) PfandBG – Extension of maturity

The 2021 Amendment introduces a paragraph 2a in section 30 PfandBG, which states that a cover pool administrator has the legal option of extending the due dates for Pfandbrief principal repayments by up to one year. The scope and duration of any extension fall within the professional discretion of the cover pool administrator.

The purpose of a maturity extension is to protect the Pfandbrief creditors by giving the cover pool administrator “time to arrange a stable funding solution and/or a transfer pursuant to sections 32, 35 (PfandBG). Alternatively, it will give the cover pool administrator time to liquidate cover assets.”4

To make use of this option, the cover pool administrator must satisfy the requirements of section 30 (2b) sentence 1 PfandBG and verify whether postponing the respective maturity date is required in order to avoid insolvency of the Pfandbrief bank with limited business activity, that the latter is not over-indebted and that it can then be assumed that, once all options for extending the due dates are implemented in full, the Pfandbrief bank with limited business activity will be solvent. If this is not the case, the cover pool administrator must initiate separate insolvency proceedings pursuant to section 30 (6) PfandBG.

The cover pool administrator may postpone principal and interest payments falling due within the first month following his appointment until the end of that period of one month. Pursuant to section 30 (2b) sentence 2 PfandBG, it can be assumed to be irrefutably established that the preconditions have been met, meaning that he is not required to perform the tests stipulated in sentence 1. This is intended to give him the opportunity to gain an overview of the financial position of such Pfandbrief bank with limited business activity.

This authority applies separately to every Pfandbrief issue. However, the extension may only be given uniformly for all Pfandbriefe of an issue, including on a pro-rata basis. To that extent, the principle of equal treatment of creditors applies.

During the extended period, the postponed principal and interest amounts bear interest in accordance with the conditions applicable up to the date of the postponement, unless stipulated otherwise in the terms and conditions of the issue.

During this extension period, the cover pool administrator may service the postponed Pfandbriefe early in accordance with section 30 (2a) sentence 7 PfandBG, for example if he receives unexpectedly high cash inflows due to early cover loan repayments.

The regulation is complicated by the “overtaking ban” based on article 17 (1) e) CBD, according to which the original sequencing for servicing the Pfandbriefe may not be changed due to the maturity extension; for frequent issuers, this is likely to result in “postponement cascades”. Section 30 (2c) PfandBG stipulates that the cover pool administrator must publicly announce extensions of maturities and early principal repayments in accordance with section 30 (2a) sentence 5 PfandBG.

The option of maturity extension applies only to Pfandbriefe, not to other liabilities of the Pfandbrief bank with limited business activity, and in particular not to derivatives, according to section 30 (7) sentence 2 PfandBG. Sentence 1 of the same paragraph clarifies that for all legal transactions entered into by the cover pool administrator, the creditors enjoy the same position as the Pfandbrief creditors, i.e., their claims are not subordinate; the purpose of such equal treatment is to make it easier to obtain new liquid funds.

In addition, the explanatory memorandum on the law makes it clear that the restrictions on postponing maturities stipulated in section 30 (2a) sentences 6 and 7 PfandBG, in particular the “overtaking ban”, apply only to Pfandbrief liabilities, i.e., not to new liabilities incurred by the cover pool administrator in the form of liquidity loans or bond issues.

According to section 6 (1) sentence 2 PfandBG, from 8 July 2022 on, a clear reference must be made in the terms and conditions of an issue to the possibility of a maturity extension and the main conditions for such an extension.

-

Sections 30 et seq. – Special provisions regarding the cover pool administrator

The 2021 Amendment adds sentence 2 to section 31 (2b) PfandBG, stipulating that the letter of appointment must indicate the legal grounds for the appointment. Indeed, the PfandBG contains several reasons for appointment. Not all “cover pool administrator variants” have the same powers. This applies, in particular, to the maturity extension, which cover pool administrators appointed in accordance with section 2 (5) and section 36a (2) sentence 5 PfandBG are not authorised to decide upon.

In order to ensure that there is no doubt about the cover pool administrator’s ability to act, Amendment I adopted in 2009 introduced the provision in section 31 (8) PfandBG, under which the cover pool administrator is entitled to make use of the staff and materials of the Pfandbrief bank and is only obliged to reimburse the insolvency estate for real costs incurred. The 2021 Amendment strengthens this, in that section 31 (8) sentence 2 PfandBG stipulates that the insolvency administrator acting on behalf of the Pfandbrief bank, at the request of the cover pool administrator, must undertake any and all actions and legal transactions required to manage the cover pools and/or refrain from any that threaten to prevent management of the cover pools.

Section 30 (6) PfandBG has been supplemented by adding the new sentence 5. This provides that in the case of advance distributions, the insolvency administrator must withhold reasonable amounts as a precaution against potential default claims in accordance with sentence 4 and that a final distribution can only be made once the possible amount of any default claims to be asserted becomes clear. The purpose of this is to prevent default claims from coming to nothing, thereby reinforcing the “dual-recourse” principle.

-

Section 41 – Protection of the name “Pfandbrief”

Pfandbriefe may only be issued by Pfandbrief banks on the basis of the PfandBG. In principle, the name “Pfandbrief” is only allowed for issues by German Pfandbrief banks. Based on aspects of European law, section 41 (2) PfandBG extends this name protection to credit institutions with head offices in other EU or EEA states whose bonds satisfy certain minimum criteria and include a reference to their origin.

The 2021 Amendment expands the name protection by adding the new section 41a PfandBG. This introduces the terms “European Covered Bond” and “European Covered Bond (Premium)”.5

Summary

The 2021 Amendment adjusts the PfandBG so that it will comply with the EU standard and will be of higher quality than the EU minimum standard. As a result, the PfandBG will continue to serve as the worldwide benchmark for laws on covered bonds. All mandatory provisions of the EU’s covered bond harmonisation are being implemented in the PfandBG. Therefore, the German Pfandbrief will also be able to continue enjoying all EU privileges.

- footnotes:

- The report from the Bundestag’s Finance Committee is available as Bundestag Publication 19/28483 of 14 April 2021.

- For more on these EU provisions, see Stöcker, EU harmonisation of Covered Bonds, Housing Finance International (HFI), Autumn 2020, pp. 38 (45 and 47).

- For a detailed discussion of the connection between LCR and the CB liquidity buffer under EU law, see Stöcker,HFI, Autumn 2020, pp. 38 (46).

- Bundestag Publication 19/26927 of 24 February 2021, page 44 (Explanatory memorandum on the law)

- For more on the connection between these names and art. 6 CBD, see Stöcker, HFI, Autumn 2020, p. 39; for more on the connection with art. 17 and art. 30 CBD, see Stöcker, HFI, Autumn 2020, p. 46.