The Pfandbrief and its legal foundations

Dr. Otmar Stöcker

Verband deutscher Pfandbriefbanken

06.2021

Investors will only provide banks with long-term capital at low interest rates if they can be certain about receiving their capital back, including the agreed interest. The purpose of issuing Pfandbriefe is to raise long-term capital at low interest rates. The German Pfandbrief Act (Pfandbriefgesetz, PfandBG) is therefore geared towards building and maintaining investor confidence. The special feature of Pfandbriefe – and the key element in creating investor confidence – is the cover securing them if the issuer becomes insolvent. This is complemented by the legal standardisation achieved by the Pfandbrief Act, the high transparency of the German Pfandbrief system and the strict supervision conducted by the German banking supervisory authority (Bundesanstalt für Finanzdienstleistungsaufsicht, BaFin).

The legal certainty created by this clear legal framework is crucial to investor confidence and the existence of a liquid Pfandbrief market. Pfandbriefe are bonds with a special security mechanism. A bond is a commitment by its issuer to pay a specific amount of principal plus interest on specific dates. Pfandbriefe may only be issued by Pfandbrief banks on the basis of the Pfandbrief Act.

Pfandbrief license

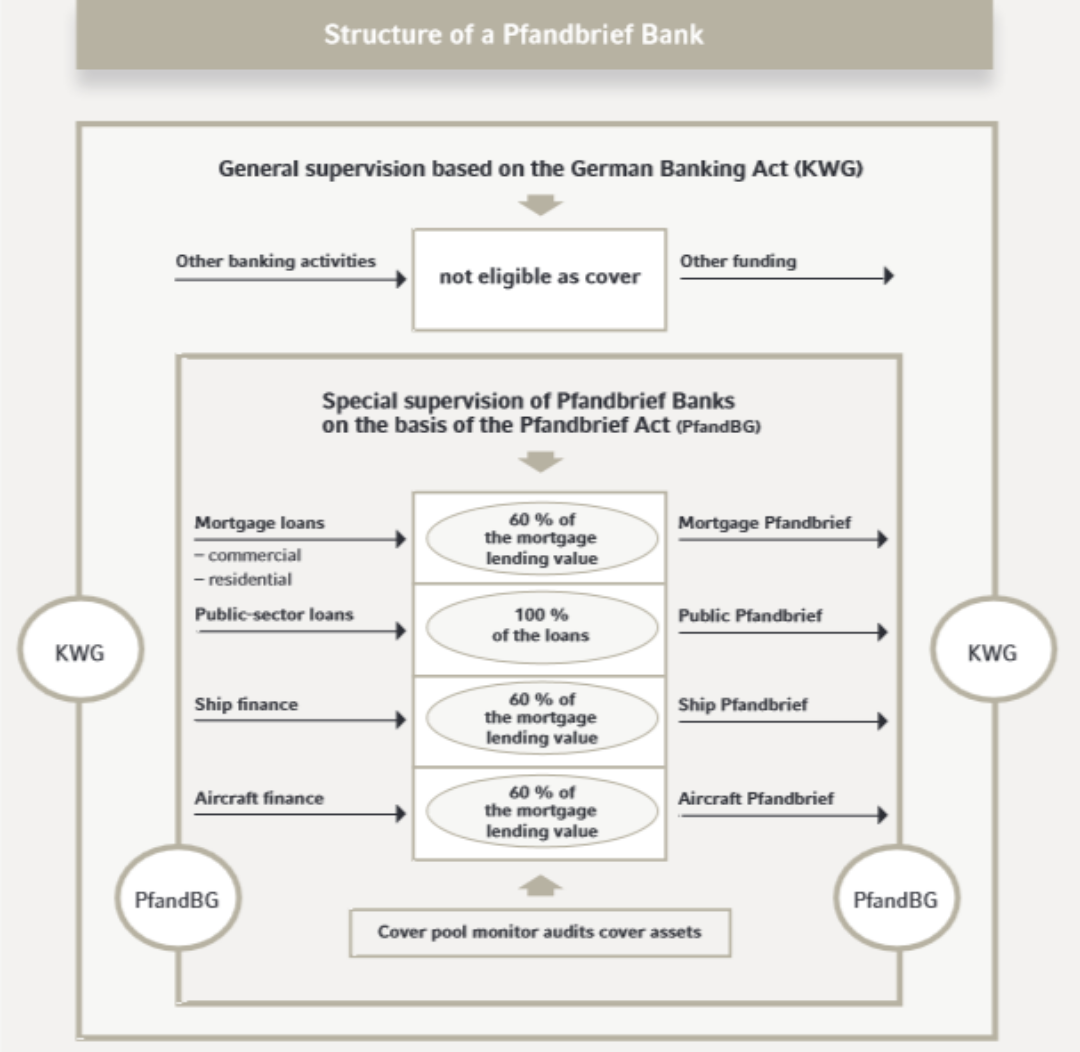

A credit institution requires a special licence to conduct Pfandbrief business, covering each type of Pfandbrief separately. Section 2 (1) PfandBG defines the individual requirements.

- The credit institution’s registered office must be in Germany.

- The credit institution must demonstrate core capital of at least 25 million euros.

- The credit institution must be licensed to lend.

- Pfandbrief banks must have a risk management system within the meaning of section 27 PfandBG that separately maps and controls the risks for the cover pool and the issuing business based thereon.

- A credit institution applying for a licence must submit a business plan to BaFin showing that it will conduct Pfandbrief business regularly and on a sustained basis and that the organisational structure required for this is in place.

- The credit institution’s organisational structure and resources must reflect its Pfandbrief business appropriately.

- Management must have the necessary knowledge in the respective areas of lending and in refinancing.

Public supervision

Public supervision of Pfandbrief banks is carried out by BaFin. This task is performed by its “Pfandbrief Competence Centre – Policy Issues and Examination of Cover Assets at Pfandbrief Banks”.

Section 5 (2) PfandBG contains a special obligation for Pfandbrief banks to send regular reports to BaFin. Accordingly, at the beginning of each calendar half-year, Pfandbrief banks must submit a list to BaFin, confirmed by their cover pool monitor, of entries made in the cover register in the previous six months.

Cover audits

In supervisory practice, cover audits – alongside ongoing supervision – are of particular importance. Pfandbrief cover must be audited regularly, approximately every three years, using suitable random samples. The costs incurred by BaFin for this audit must be reimbursed by the Pfandbrief bank. Cover audits are carried out by BaFin itself or by external auditors; in the latter case, this is put out to public tender.

Cover audits comprise random checks of individual cover assets and their legal eligibility as cover, and – in the case of Mortgage Pfandbrief cover assets – a valuation of the mortgaged property based on mortgage lending value principles.

Note, however, that BaFin does not have to check whether the necessary cover is in place before every issue; this is the cover pool monitor’s task.

Cover pool monitor

Each Pfandbrief bank requires an independent cover pool monitor, appointed by BaFin, and at least one deputy. The appointment, dismissal and duties of the cover pool monitor are governed by sections 7 to 11 PfandBG.

The cover pool monitor is appointed by BaFin after consultation with the Pfandbrief bank. Cover pool monitors are not bound by BaFin instructions but must provide it with information on their findings and observations. Cover pool monitors are tasked with ensuring that the prescribed cover for Pfandbriefe and claims under derivatives is in place at all times.

One of the cover pool monitor’s tasks is to confirm, before issuance, that the Pfandbriefe have the prescribed cover and that the cover assets have been entered in the corresponding cover register. This confirmation can also be made digitally in the case of electronic issues since the Act on the Introduction of Electronic Securities came into force. Furthermore, a cover asset may only be deleted from the cover register with the cover pool monitor’s consent.

The Pfandbrief Act requires cover pool monitors to have the knowledge and experience necessary for their tasks. This is presumed to be the case if they are qualified as an auditor or chartered accountant. Pfandbrief banks must pay the cover pool monitor appropriate remuneration, the amount of which is set by BaFin, and any necessary expenses.

Cover principle

The cover principle is crucial to the security of Pfandbriefe. Throughout the term of a Pfandbrief, the resulting liabilities must be adequately covered by assets, i.e. assets must exceed liabilities to the extent stipulated by law. This is also referred to as statutory over-collateralisation (section 4 par. 1 PfandBG). If an issuer defaults, these assets must be used to repay the capital and interest of the Pfandbrief on a priority basis. To this end, strict requirements are in place regarding the type and quality of cover assets.

Upon the issuer’s default, cover assets are prioritised for repayment of capital and interest according to the extensive and detailed provisions of the separation principle (section 30 PfandBG). The matching principle ensures that sufficient cover assets are in place at all times throughout the term of the Pfandbriefe.

Cover and the matching principle must be considered separately for each Pfandbrief type. The individual Pfandbrief types of an issuer are not linked to each other. For example, over-collateralisation in the Mortgage Pfandbrief cover pool cannot be used to secure Public Pfandbriefe. Instead, the cover requirements for each type of Pfandbrief must be fulfilled separately.

Pfandbrief issues are usually larger than individual loans, and payment dates on the asset and liability sides are not fully congruent. The Pfandbrief Act does not set any detailed limits in this regard but does contain several provisions to ensure matching cover.

Cover pools

The special status of cover assets in the event of the issuer’s insolvency is conferred by their entry in the cover register. The cover register is maintained by the Pfandbrief bank, with a separate section for each type of Pfandbrief, and is monitored by the cover pool monitor. Assets entered in or legally belonging to the register form a separate asset pool and do not belong to the general insolvency estate of the issuer or Pfandbrief bank. The register’s purpose is to enable these assets that are exempted from inclusion in the insolvency estate to be identified in the event of insolvency. The assets entered in the cover register are called cover assets and, collectively, a cover pool.

Pfandbriefe in circulation must be covered according to their net present value – including interest and amortisation obligations – and nominal value. Using suitable calculation tools, the Pfandbrief bank must ensure at all times that this prescribed cover is in place and documented comprehensibly; this is called the cover calculation.

The concept of net present value cover was introduced to manage interest rate cover and currency mismatches: interest rate and currency fluctuations in the cover must withstand stress scenarios, the details and methodology of which are prescribed by BaFin in the German Net Present Value Regulation (Pfandbrief-Barwertverordnung, PfandBarwertV). The net present values of foreign currency positions must be converted into euros at the respective prevailing exchange rate. These stress tests must be documented by the Pfandbrief bank.

180 days liquidity buffer

In order to safeguard the cover pool’s liquidity, section 4 (1a) PfandBG stipulates that Pfandbrief banks must, on a same-day basis for the next 180 days, reconcile claims falling due under cover assets and liabilities from outstanding Pfandbriefe against each other. The largest cumulative liquidity gap thus calculated must be covered by liquid assets.

Risk Management

The risk management system prescribed by general banking law is an existing mechanism for taking account of the risks associated with the Pfandbrief business. Section 27 PfandBG reiterates this and details the specific requirements for safeguarding investors’ interests.

Section 27 (2) sentence 1 PfandBG stipulates that the system must be able to identify, assess, control and monitor all related risks. The following risks are mentioned: counterparty, interest rate, currency and other market price, operational and liquidity risk. Limit systems should be used to prevent cluster risk, among other risks, and a risk report must be submitted to the Management Board at least quarterly.

No separate risk management system is required for this if the Pfandbrief bank as a whole has a system separately showing the specific risks of Pfandbrief business. Section 27 (2) sentence 1 PfandBG stipulates that Pfandbrief banks must carry out and document a comprehensive risk analysis for transactions in new products, types of business or new markets. A Pfandbrief bank may not include assets in cover until it has obtained sound expert knowledge, and in the case of mortgage lending must wait for two years; in all cases, the existence of sound expert knowledge must be detailed in writing.

Types of Pfandbrief

German law provides for four types of Pfandbrief, depending on the underlying cover business:

- Mortgage Pfandbriefe for funding real estate mortgage loans,

- Public Pfandbriefe for loans to the state or local authorities or for loans secured by guarantees from the state or local authorities,

- Ship Pfandbriefe for ship mortgages and Aircraft Pfandbriefe for aircraft mortgages.

Sections 12 to 19 PfandBG set out the requirements for cover assets for Mortgage Pfandbriefe.

Mortgage Pfandbrief

Eligible cover assets are claims secured by security rights over real property, whose value must be recoverable. “Mortgages” (section 12 (1) PfandBG) are suitable cover. The Pfandbrief Act mentions ”mortgage” in many places. A conventional term in Pfandbrief legislation, this means that the cover asset is the loan claim secured by a security right over real property.

The security right over real property must encumber a property. Both commercial and residential properties are suitable for this. The Pfandbrief Act does not stipulate the loan’s intended use for it to be eligible as cover, but only those parts of the claim and the security right over real property that do not exceed 60% of the mortgage lending value will be considered for cover.

Real estate is property and other rights equivalent to real property. Under German law, a building is an essential part of a property; examples of other rights equivalent to real property include leasehold and condominium ownership.

Under section 1 (1) no. 1 PfandBG, security rights over real property that are used as cover must be the Pfandbrief bank’s own security rights over real property. However, section 1 (2) PfandBG permits mortgages held in a fiduciary capacity by another, suitable credit institution to be used as cover, provided the Pfandbrief bank has an insolvency-proof position. This is the case if the Pfandbrief bank has a claim against final transfer of the security rights over real property and the latter are deemed to belong to the Pfandbrief bank in the event the other credit institution becomes insolvent or compulsory enforcement measures are taken against it. This issue is particularly important in syndicated and portfolio financing, as well as in pooling models.

In German law, this is achieved through the funding register. If the fiduciary bank becomes insolvent, the beneficiary (in this case the Pfandbrief bank) has a right to segregation for items entered in the funding register maintained by the fiduciary bank.

If buildings firmly connected with the property are deemed to increase the mortgage lending value, it must be ensured throughout the term of the loan that, should any such building be damaged or destroyed and not restored, the Pfandbrief bank receives indemnity under an insurance policy. As a minimum, insurance must cover significant risks in terms of the property’s location and type.

The mortgaged property must be located in a member state of the European Union (EU) or European Economic Area (EEA), Switzerland, the United Kingdom of Great Britain and Northern Ireland, non-European G7 countries (i.e. USA, Canada and Japan), plus Australia, New Zealand or Singapore.

The total volume of cover assets in non-EU states for which preferential rights in insolvency of Pfandbrief creditors are not ensured may not exceed 10% of the cover assets for which preferential rights are ensured.

In order to secure Mortgage Pfandbriefe, and in particular to facilitate liquidity management, other assets, e.g. government bonds and claims against credit institutions, may be included as cover within limits.

Umfang.

Mortgage Lending Value

The main elements of collateral for Mortgage Pfandbriefe are the valuation, lending value and lending limit. The basis for valuing the property serving as cover is section 16 PfandBG and the Regulation on the Determination of Mortgage Lending Values (Beleihungswertermittlungsverordnung, BelWertV).

In principle, a Pfandbrief bank is free to grant a mortgage loan in any amount, regardless of the property’s value. However, the value of claims from mortgage loans that can be used as cover for Pfandbriefe, and thus be refinanced by Pfandbriefe, cannot exceed 60% of the mortgage lending value.

Public Pfandbriefe are used to refinance claims against the state and government institutions. The most important difference compared with Mortgage Pfandbriefe is that loans to the state and local authorities are not secured by mortgages but are based on the public sector being solvent at all times.

Public Pfandbrief

Section 20 PfandBG sets out the requirements for cover assets for Public Pfandbriefe. Cover assets must be monetary claims. German local authorities are an example of eligible debtors of monetary claims, which must be direct claims against the debtor.

Entities eligible as foreign public debtors include all EU member states, i.e. central governments, central banks of these states, regional administrations and local authorities. The same applies to EEA member states. As in the case of EU member states, eligibility of the above-mentioned entities as debtors is not subject to any further restrictions, for example with regard to the public debtor’s credit quality. In contrast, public debtors from Switzerland, the USA, Japan, the United Kingdom of Great Britain and Northern Ireland, and Canada must be assigned to credit quality step 1; this requires a specific minimum rating.

Some years ago, the vdp developed a credit quality differentiation model. This voluntary self-regulation is designed to supplement the statutory cover requirements with rules for value deductions from cover claims with low credit quality. Pfandbrief banks are therefore stricter than general banking supervisory law requires.

In addition to direct claims, monetary claims guaranteed by certain government bodies are also eligible as cover, e.g. municipal guarantees. Export credit agencies domiciled in an EU or EEA state, the USA, Japan, Switzerland, the United Kingdom of Great Britain and Northern Ireland or Canada may also be eligible guarantors under certain conditions.

Section 28 disclosure

Pfandbrief banks are subject to wide-ranging transparency regulations. They must publish extensive quarterly information on both their Pfandbrief and cover business. The purpose is to ensure that Pfandbriefe are comparable and that investors have optimum information for assessing them.

Issuers under the vdp umbrella have enhanced their transparency beyond the requirements of section 28 by providing individual and aggregated data on the vdp website in file formats that can be further processed. Most vdp member institutions also voluntarily publish more detailed data, which can also be accessed via the vdp website.

Pfandbrief holders’ preferential right

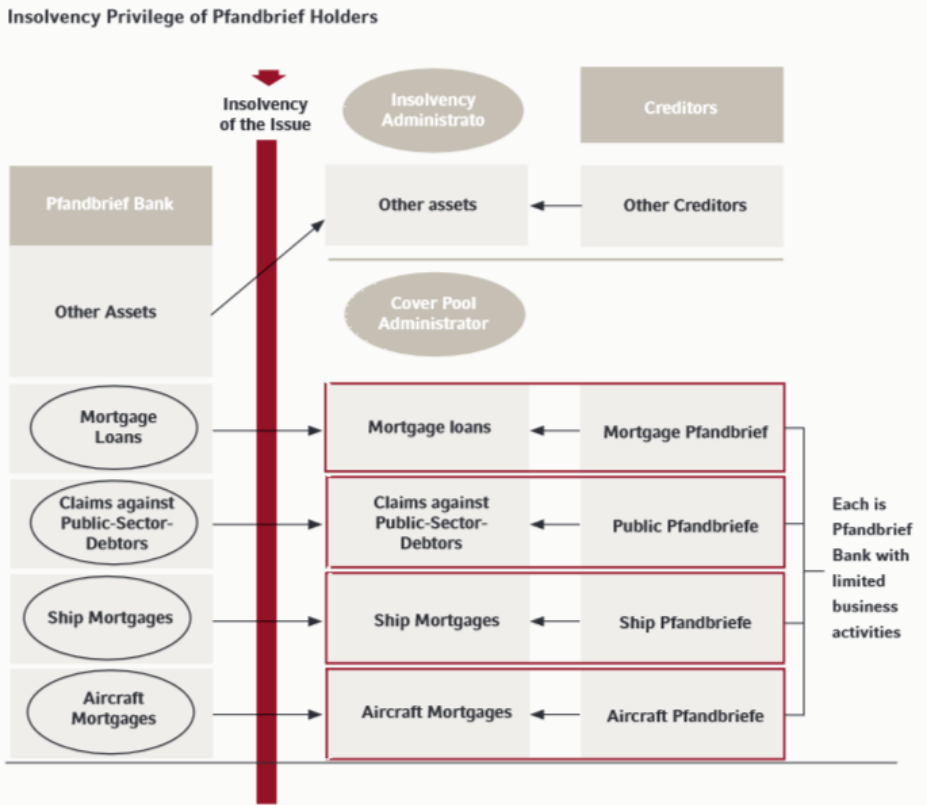

The core of the Pfandbrief system is the preferential right of Pfandbrief holders in the event of the issuing Pfandbrief bank becoming insolvent. This is regulated in sections 30 to 36a PfandBG.In principle, all liabilities of an insolvent debtor fall due in the event of insolvency (section 41 (1) of the German Insolvency Act (Insolvenzordnung, InsO)). Section 30 (1) sentence 2 PfandBG is an exception to this: Pfandbriefe do not fall due if their issuer, i.e. the Pfandbrief bank, becomes insolvent. The provisions of the Pfandbrief Act are designed to ensure that, even if the Pfandbrief bank becomes insolvent, Pfandbrief holders receive the agreed capital and interest payments in full and on time, i.e. as contractually agreed.

If a Pfandbrief bank becomes insolvent, the cover pools and respective Mortgage, Public, Ship or Aircraft Pfandbriefe do not become part of its insolvency estate. Instead, they form, separately for each Pfandbrief type, ”assets of the Pfandbrief bank that are exempted from inclusion in the insolvency estate”.

However, with the opening of the insolvency proceedings, there is an automatic separation of the assets into a part subject to the insolvency proceedings (and the Pfandbrief bank’s insolvency administrator) and a part subject to the special provisions of §§ 30 et seq. of the Pfandbrief Act (and the Pfandbrief bank’s cover pool administrator); this part is called “Pfandbrief bank with limited business activity” (Pfandbriefbank mit beschränkter Geschäftstätigkeit). In order to fully satisfy the claims of Pfandbrief creditors, the cover pool administrator may, with effect for the cover pools, conclude any legal transactions required for an orderly resolution of the cover pools. The legal entity of Pfandbrief bank retains legal title to the cover pools; there is no separation under German company law.

Maturity extension

With the amendment to the Pfandbrief, the German legislator has regulated with effect from 1 July 2021 that a cover pool administrator may postpone the maturity of a Pfandbrief issue by up to 12 months under certain conditions (section 30 paras. 2a and 2b PfandBG). In this context, a “ban on overtaking” must be observed, according to which the order of redemption of issues must not be changed. The possibility of extending the maturity applies both to Pfandbriefe issued before 1 July 2021 and to new issues. In the first month after the appointment of the cover pool administrator, the latter may postpone the accruing interest and redemption payments to the end of this period, assuming by law that the necessary requirements are met. A postponement of the redemption payment beyond this point in time is only possible if the cover pool is not overindebted, the extension is necessary and the cover pool administrator may assume that he will be able to service the bond after the extension period.

However, when insolvency proceedings are opened, the assets are automatically separated into a part subject to the insolvency proceedings (and the Pfandbrief bank’s insolvency administrator) and a part subject to the special provisions of section 30 et seq. PfandBG (and the Pfandbrief bank’s cover pool administrator). The cover pool administrator therefore also acts for the Pfandbrief bank, i.e. for the part not subject to insolvency proceedings.

If, during the resolution procedure, it becomes apparent that the cover pool is insolvent or over-indebted, separate insolvency proceedings will be opened at BaFin’s request against the assets of the Pfandbrief bank with limited business activity. These insolvency proceedings will then be subject to insolvency legislation, with the cover pool administrator replaced by an insolvency administrator.

Resolution

Pfandbrief creditors can assert claims for a potential default in insolvency proceedings against the Pfandbrief bank’s general assets. Resolution legislation – the EU Bank Recovery and Resolution Directive (BRRD) and its implementation into German law by the German Recovery and Resolution Act (Sanierungs- und Abwicklungsgesetz, SAG) – provides resolution authorities with extensive powers and several resolution tools.

One of the tasks of the resolution authorities – the Single Resolution Board (SRB) and BaFin – is to draft resolution plans in preparation for a crisis situation. These resolution plans also include the Pfandbrief and cover business of Pfandbrief banks.

Section 36a PfandBG, which contains a number of provisions for crisis situations, serves to coordinate resolution legislation and Pfandbrief legislation. Resolution legislation also stipulates that the resolution tool of writing down liabilities does not apply to Pfandbriefe in so far as they are covered.