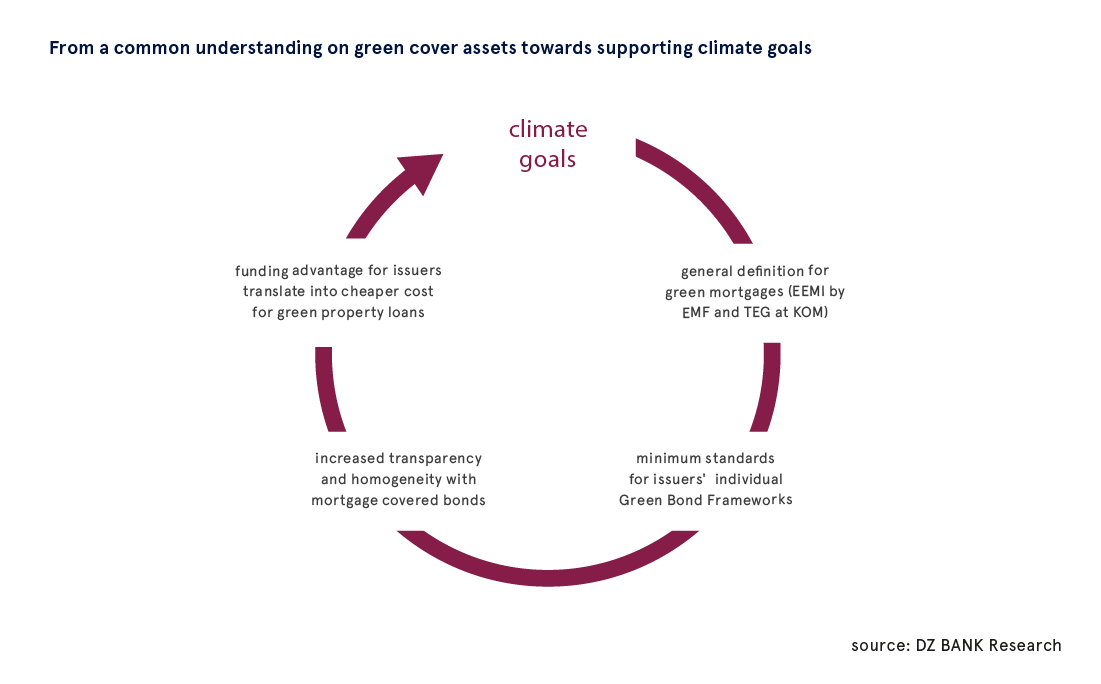

Minimum standards for Green Pfandbriefe show that Pfandbrief banks are actively committed to achieving climate objectives

Sascha Kullig

Association of German Pfandbrief Banks

08.2019

August 2019

German Pfandbrief banks are committed to climate objectives and want to play their part in making sure that the carbon savings envisaged for the building sector can be achieved. As of 2019, the Association of German Pfandbrief Banks (vdp) has central responsibility for administering trademark rights to the “Green Pfandbrief” product for and on behalf of its member institutions. This will ensure rigorous ongoing development of the still young market segment. To this end, Pfandbrief banks belonging to the Association and active in the segment have formulated minimum standards for the issuance of green Mortgage Pfandbriefe. These are Mortgage Pfandbriefe secured by green real estate loans. This means that all provisions of the German Pfandbrief Act also apply to Green Pfandbriefe.

The standards take account of the initiatives being formulated at EU level for the introduction of a “taxonomy” for sustainable economic activities and an EU Green Bond Standard. They include requirements for the energy efficiency of financed buildings and oblige Pfandbrief banks to maintain a high degree of transparency. Investors can therefore rest assured that all Green Pfandbriefe meet high sustainability standards.

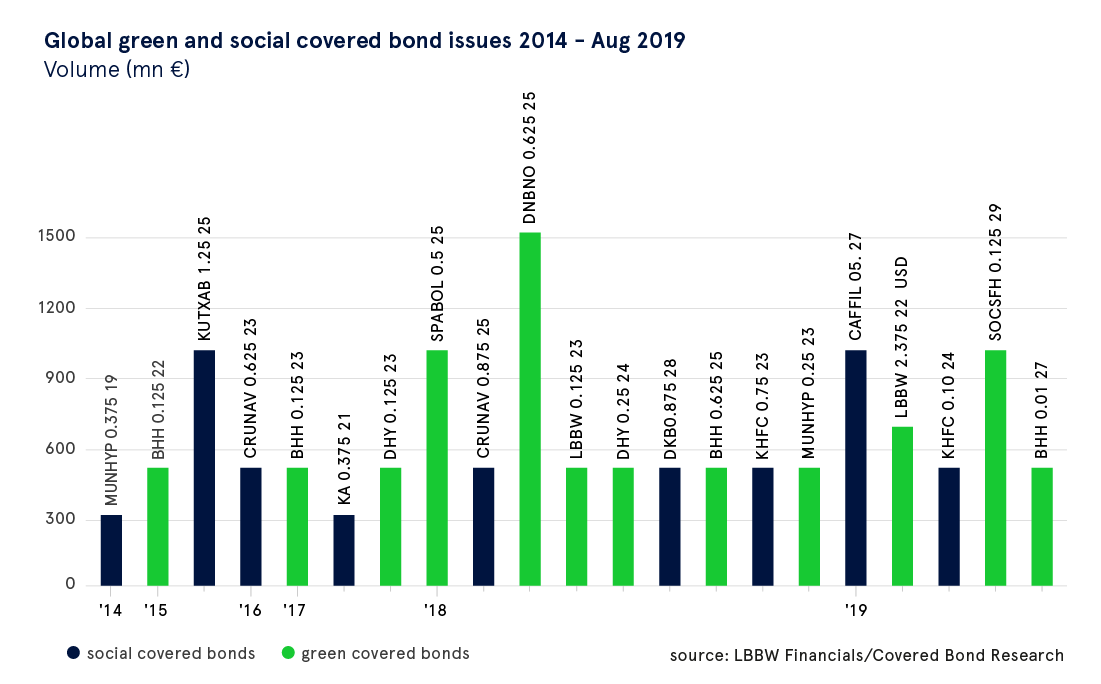

Green Pfandbriefe are market leaders in Europe

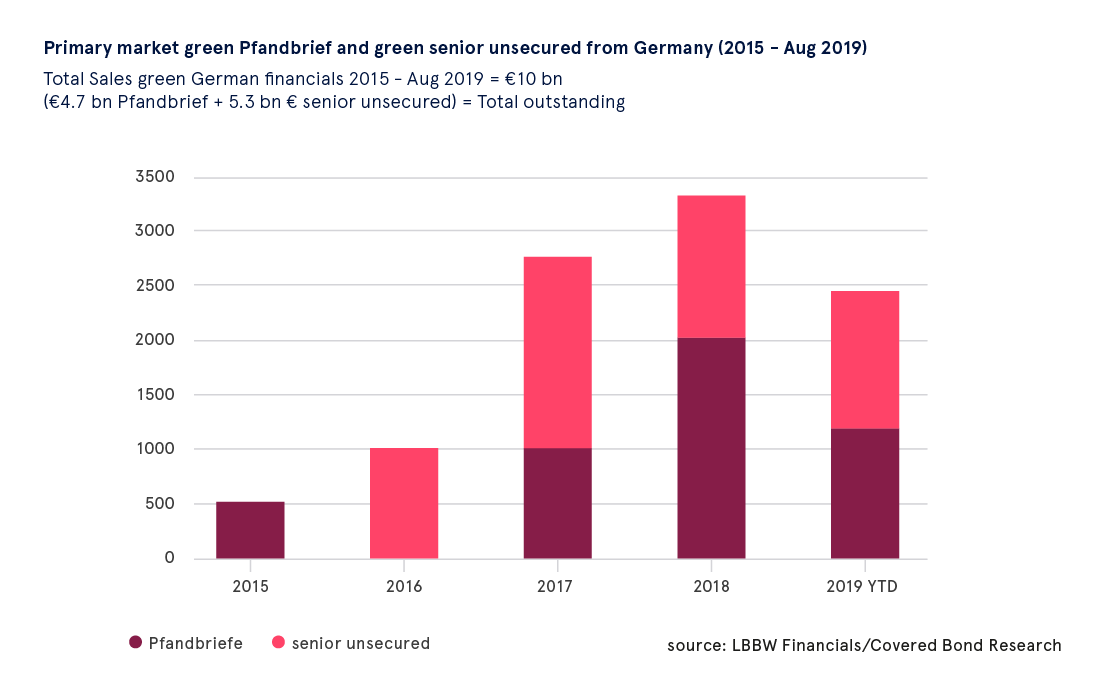

Pfandbrief banks are already among the most active banks in Europe for sustainable bond issues. They issue unsecured green bonds and also environmentally sustainable, green or social Pfandbriefe. They are world leaders in the Green Covered Bonds segment, with an issuance volume of around 5 billion euros at mid-2019. The market leader is BerlinHyp, which also previously owned the rights to the name “Green Pfandbrief”. This year it transferred these rights to the Association of German Pfandbrief Banks (vdp). The minimum standards now in place will give the segment a further boost.

A high degree of transparency

Transparency plays an important role in this respect since investors want to know what they are investing in. Pfandbrief banks are therefore committing themselves to publishing detailed information about Green Pfandbriefe. In particular, this includes information on the qualifying assets in the cover pool, the issuer’s “Green Bond Framework” and the “second party opinion” prepared by a qualified independent party. Issuers active in the Green Pfandbrief segment regularly publish all this information on their websites.

The Green Bond Frameworks of the German Pfandbrief banks are all based on the Green Bond Principles of the International Capital Market Association (ICMA), which have become the market standard. The Principles call on issuers to set out regulations on the use of issuance proceeds, individual project selection, revenue management and reporting. Hence, they primarily create a framework for Green Bonds, while specific requirements are defined individually.

Pfandbrief banks take quite different approaches when it comes to the details, but essentially the focus is on energy consumption and demand. For example, most banks have set upper limits for the energy consumption and demand of buildings, depending on the type of building. Energy performance certificates are often used as proof. However, since these are not always available, the minimum standards also accept a ranking in the top categories of certain sustainability certificates.

Another alternative is to require the property to be in the 15% of the national property stock with the lowest energy consumption or demand. For residential real estate, co-financing by KfW funding programmes for energy-efficient construction and renovation may also be used as a criterion.

Investors are interested not only in how banks use the issuance proceeds, but above all in the contribution their investments actually make to climate protection. Against this backdrop, impact reporting has become increasingly important. The minimum standards therefore also include an obligation to draw up and publish an annual impact report.

Commitment to climate protection targets

Pfandbrief banks are committed to the goal agreed at the 2015 Paris Climate Conference of limiting global warming to a maximum of 2 degrees centigrade. According to the German government’s climate protection plan, the building sector in Germany is expected to reduce its carbon emissions to around 70 million tonnes in 2030 and become CO2 neutral by 2050. Pfandbrief banks can only make an indirect contribution to achieving the climate targets, since they do not build or renovate buildings themselves. What they can do, however, is create incentives for energy-efficient buildings when financing such projects. This applies to both commercial and residential real estate. As a result, a few Pfandbrief banks offer “green” real estate financing, whereby they offer their customers more favourable terms than with conventional real estate financing.

Incentives needed for building refurbishment

In the current market environment, however, such offers are not easy to make. That is due, on the one hand, to the already low level of interest rates and to intense competition, which leads to low margins. In addition, borrowers are often unwilling to provide comprehensive information on the energy efficiency of the property to be financed. Banks thus do not always have sufficient data to assess the building’s energy rating, particularly as energy performance certificates do not always exist despite the legal requirement. A central web-based and freely accessible register could be a great help here.

Quite apart from data availability, there is a further problem: energy-optimised refurbishment of a building is often not very attractive for the owner. The costs of a building refurbishment often exceed the combined total of the value enhancement and the savings from lower heating costs. More favourable terms from Pfandbrief banks are not able to close this gap either. Rather, government incentives are needed so that as many property owners as possible can actually contribute to achieving climate targets.

European initiative to strengthen green real estate financing

Pfandbrief banks are trying to make the financing of green properties more popular despite all these uncertainties. They are part of the “Energy Efficient Mortgage Initiative” led by the European Mortgage Federation and financed by the European Commission. The initiative’s aim is to promote a common definition of green real estate financing. Furthermore, relevant data is to be gathered and analysed to determine whether green real estate generally has a lower probability of default and/or loss given default than conventional real estate financing. If this is the case, lower equity requirements could be justified for green property financing. The necessary analysis will not be easy and will take time. In particular, data availability presents a major challenge here too. Patience is thus required.

Regulatory policy must facilitate rather than hinder

The industry initiatives are evidence of strong market momentum. This must not only be maintained but also strengthened. Regulatory activities can contribute to this. However, they could also do the opposite. As always, it is a fine line. The regulatory initiatives of the European Commission are a prime example of this. This subject justifiably enjoys top priority at EU level, and so the Pfandbrief banks not only welcome the “EU Action Plan on Financing Sustainable Growth”; in principle they also consider most of the European Commission’s proposed regulations published under the action plan to be sensible. However, the amendments requested by some MEPs to the proposed regulations on publication requirements, benchmarks and taxonomy in particular have shown how quickly the necessary sense of proportion can be lost.

Furthermore, the devil is famously in the detail. With regard to the “taxonomy”, the goal of supporting the market with the help of a common understanding of green activities whilst at the same time preventing the dreaded “greenwashing” is no doubt shared by almost everyone. The question is, what is green and who decides? The Technical Expert Group (TEG) set up by the European Commission has proposed technical criteria for environmentally sustainable economic activities in various sectors, initially focusing on the two targets of climate protection and adaptation to climate change. Whereas in the first TEG proposal the technical criteria for the building sector only covered new construction and renovation, and were also extremely ambitious, the revised proposal published in June 2019 also takes existing financing into account. Furthermore, the TEG recognises the scale of the transformation needed to achieve the eventual climate targets and has formulated a suitably wide range of technical criteria. It is important that the criteria should take existing industry initiatives into account and be practical as well as ambitious, but they should not set the bar too high from the outset. Otherwise, “shifting the trillions” risks becoming “searching for the millions”.

Coordination instead of cacophony

This risk is exacerbated by the fact that legislators, central banks, standard setters and multilateral organisations at all levels, i.e. national, European and worldwide, are tackling these issues and thinking about rules at the same time. Things are changing so fast and in so many places that credit institutions are presumably not the only ones feeling a little giddy and hardly knowing which way to turn. This development is counterproductive as it deters interested parties from committing to the segment. To mute the cacophony, all key players should coordinate their activities in this area.

Pfandbrief banks and their Association are helping to achieve the Paris climate targets. The Pfandbrief can play an important role in this process, since it converts theoretical objectives into practice in a unique way. It connects the granting of loans – such as real estate loans to private house builders – with the investment decisions of institutional investors, so it can play its part on both sides in channelling as much private capital as possible into the attainment of climate objectives. Not for the first time in its 250-year success story, the Pfandbrief shows that tradition and innovation can go hand in hand.