Fitch’s View: Climate Change and Credit Risk for Covered Bonds

Sebastian Seitz

Fitch Ratings

Carmen Munoz

Fitch Ratings

03.2020

To date, environmental factors have not had a significant positive or negative impact on Fitch’s covered bond (CVB) ratings. An increasing number of countries across the world have been issuing policies to tackle climate change and yet they have only had impact on the credit ratings of a handful of sectors, most notably the utility sector. Bank lending policies have also been evolving with loans being channelled to more energy efficient residential and commercial properties with energy performance certificates of ‘A’ and ‘B’. Many of these policies have not been financially demanding for issuers within the rating horizon or have been limited in scope.

In the future we may see positive developments from environmental considerations, particularly if they improve collateral and borrower quality and these flow through to lower credit enhancement levels or overcollateralization (OC) for particular rating levels. Currently Fitch still does not differentiate between energy and non-energy efficient mortgages when rating “Green” covered bonds and RMBS as there is no historical data available evidencing a better performance for those considered to be energy efficient. In some instances we also note that, even if certain loans have been identified for the purpose of the green issuance, they could have already been in the cover pool and considered in our stressed asset analysis, indicating that it is still early times for surfacing evidence of any impact from green issuances.

In the Netherlands we have also identified “Green” RMBS issuance where a large proportion of the cover pool consists of NHG mortgages (Nationale Hypotheek Garantie; public mortgage loan insurance scheme in the Netherlands). In this case we do have evidence that the borrowers with these mortgages perform better and, where this is the case, we have assigned a positive environmental, social and governance relevance score (ESG.RS) of ‘4 (+)’ or ‘5 (+)’ in the social category of “Human Rights, Community Relations, Access & Affordability”.

As captured in criteria, when assigning ratings to US RMBS transactions, Fitch incorporates adjustments to its loan loss expectations to reflect catastrophe risk. We licensed AIR Worldwide Corporation’s CATRADER natural catastrophe model to estimate residential property damage in 10,000 different disaster scenarios across every county in the US. The output of the model is used to estimate the probability of different levels of property loss due to natural disasters, and we use this to reduce each loan’s current property value when projecting credit losses. While most US RMBS transactions benefit from high diversification and low concentration in areas prone to environmental catastrophes and are scored at a baseline of ‘3’ for “Exposure to Environmental Impacts”, transactions receiving modelled property value haircuts between 1.5-2.0% are scored a’4’ and those above 2.0% are scored a ‘5’.

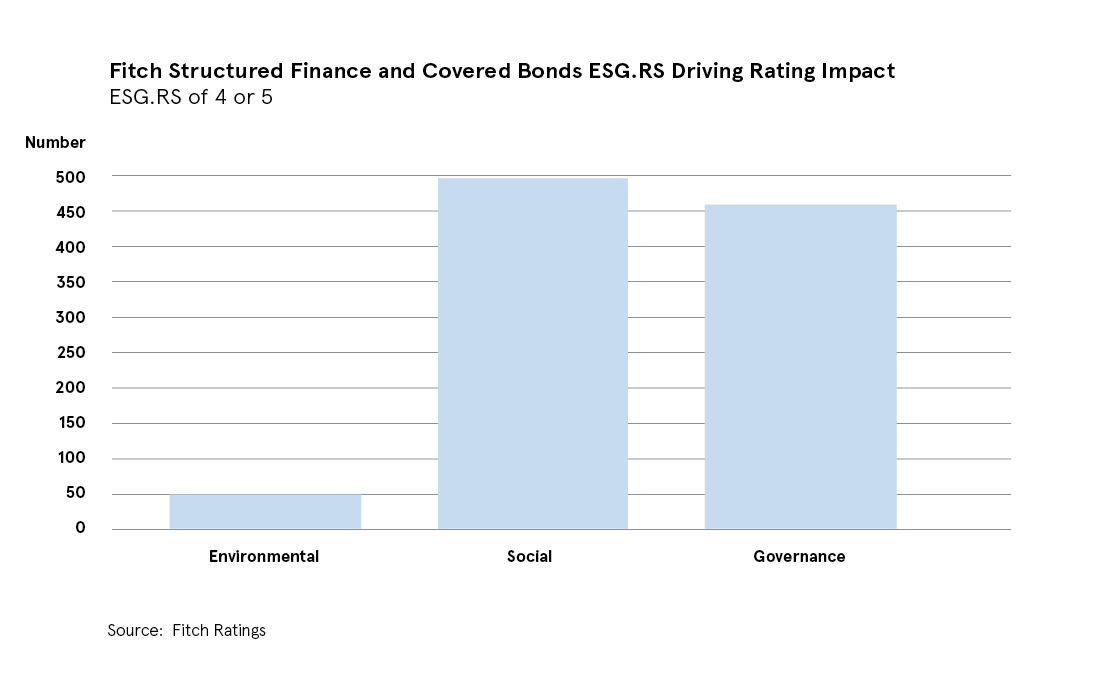

In our 4Q19 launch of ESG.RS for structured finance and CVB, we identified Governance factors as being the key driver of negative ESG factors for CVB ratings, and Social factors as being the key driver of positive scores.

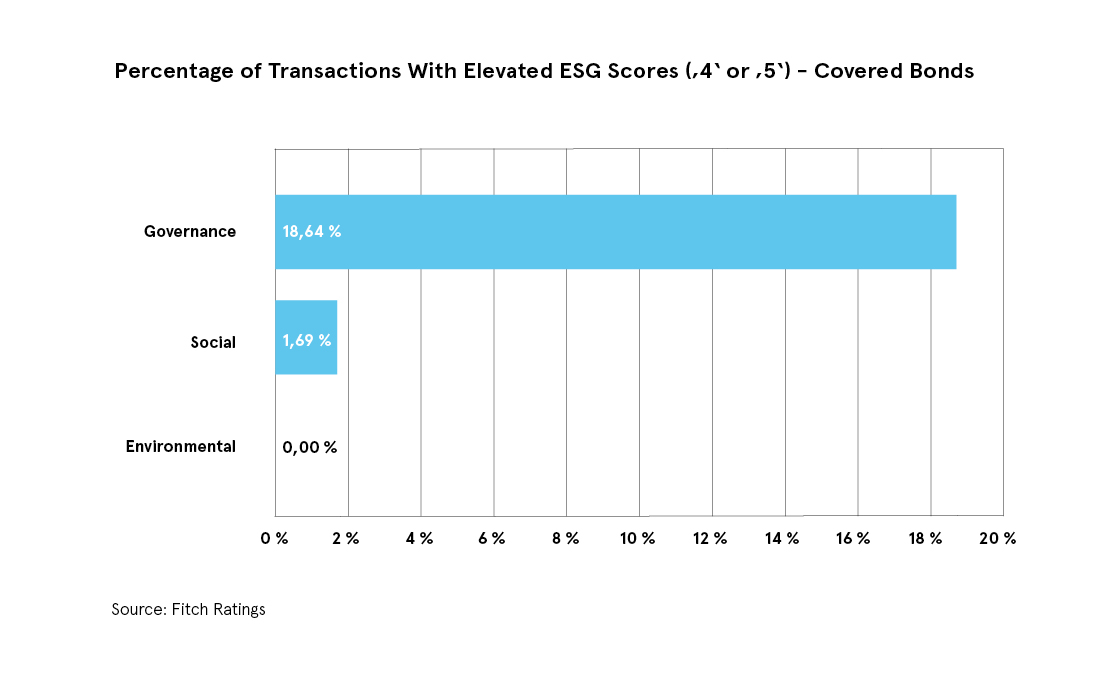

Around 20% of the CVB programs (including Multi-Issuer Cedulas Hipotecarias transactions) rated by Fitch globally received at least one elevated ESG.RS of ‘4’ or ‘5’. This implies that only in these circumstances were they relevant to ratings either alone or in combination with other factors. Governance factors in southern Europe, mainly relating to Spanish and some Portuguese CVBs which lack liquidity protection mechanisms, were the main reason for this and have limited the maximum achievable uplift we can assign above the bank’s Issuer Default Rating (IDR). This alone has had a direct Rating impact despite protection through OC. These elevated scores are likely to be lowered once the EU Covered Bond Directive is transposed into national law as it includes mandatory 180-day liquidity coverage which would mitigate the risks that are resulting in the currently elevated ESG.RS for these transactions.

The German Climate Package

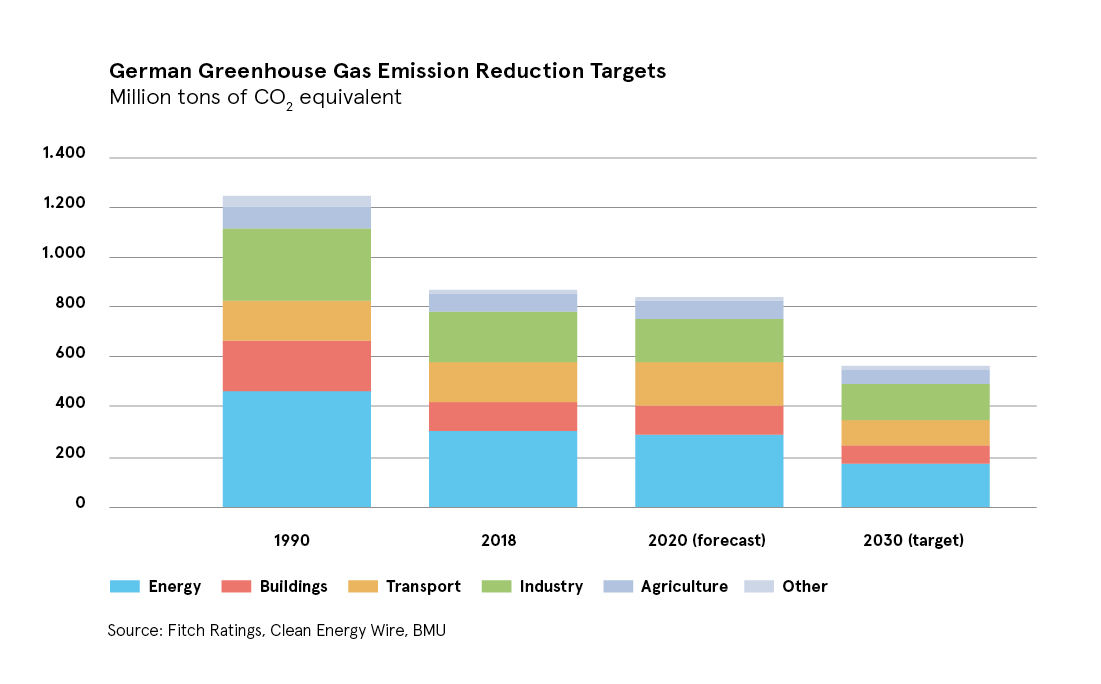

In a recent publication by Fitch, we noted that the German 2030 climate package may become a blueprint for other national environmental regulations. The package includes the first comprehensive federal law, which created a framework and legally binding sector targets, as well as the Climate Action Programme 2030, which prescribes measures and support programmes that will be legislated at a later date in sector-specific and regional laws.

Among the areas identified is the more climate friendly “Building and Living” features with a mix of incentives, CO2 pricing and regulatory measures. Tax breaks exist for energy-efficient renovation such as replacing central heating, fitting new windows, and insulating roofs and outside walls which are partially tax deductible from 1 January 2020. Also, the German government will reimburse up to 40% of the costs of swapping oil-fired heating systems for more efficient ones.

Environmental factors could impact more on ratings if commitments made are turned into actions, and if these measures translate into enhanced performance by borrowers taking out mortgages. Should borrowers’ willingness and ability to pay mortgages improve, this would be reflected in Fitch lowering its asset stresses and, if this were the case, we would expect to see positive elevated ESG.RS for the bonds issued against the collateral.

Steps to the right direction are also embodied in the European Mortgage Federation – European Covered Bond Council [EMF-ECBC] work on the development of an “energy efficient mortgage” according to which building owners are provided with incentives to improve the energy efficiency of buildings or acquire energy efficient properties with beneficial funding conditions. This initiative has support of a major group of EU banks, mortgage banks and data providers, among others, with the intention of addressing the fragmented regulatory and disclosure standards across Europe and fomenting and develop private financing of energy efficiency. The Energy Efficient Mortgages Initiative (EEMI), as the project is known, consists of two parallel projects, the Energy efficient Mortgages Action Plan (EeMAP) and the Energy Efficient Data Portal & Protocol (EeDaPP).

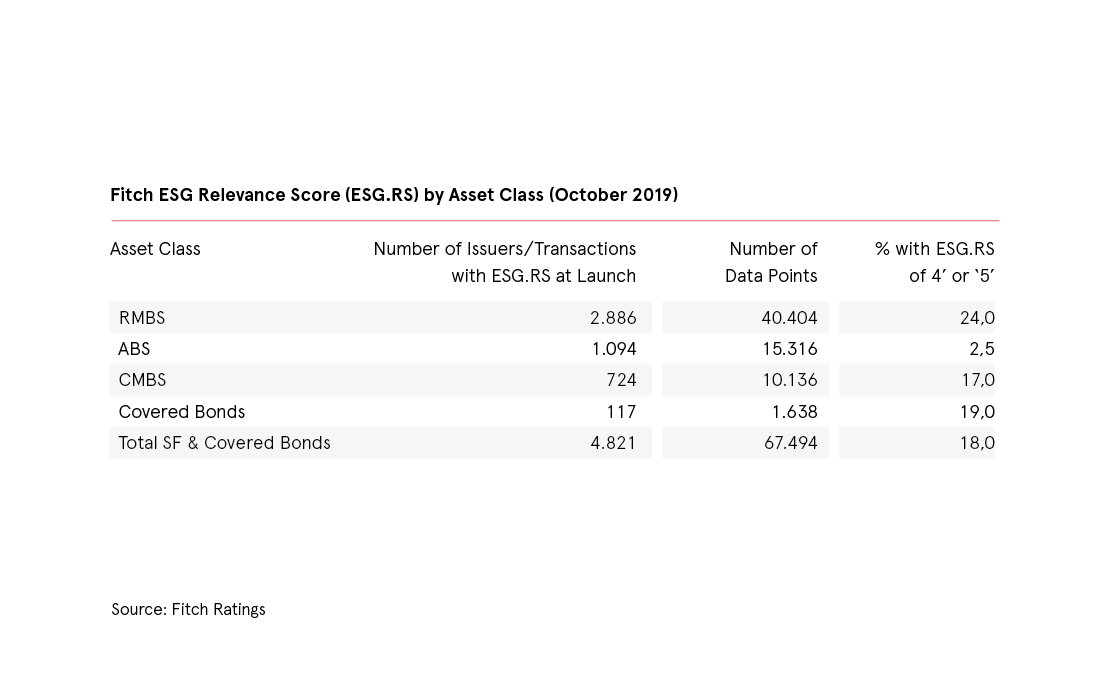

Fitch’s approach to ESG

In 2019, Fitch released more than 143,000 ESG.RS for over 10,200 issuers and transactions across Corporates, Financial Institutions, Sovereigns, Public Finances, Infrastructure, Structured Finance and Covered Bonds. In the case of SF and CVB, this meant over 67,000 ESG.RS for 4,821 SF transactions and CVB programs. The ESG.RS scores indicate the relevance and materiality of 14 ESG factors to SF and CVB ratings as expressed in the scoring definition (shown in the table in below right). By assigning elevated ESG.RS of ‘4’ or ‘5’, Fitch analysts are able to highlight those factors that were deemed particularly relevant and, therefore, influential to a rating decision. ‘4’ or ‘5’ scores can be positive or negative.

Our ESG.RS for SF transaction and CVB programs were built using a transaction / program level system to assign scores to bonds that are publicly rated on an international rating scale. The scores were assigned independently of, and in the majority of cases deviate from any ESG.RS assigned to the originators or issuers.