Implications from the IBOR-Benchmark Reform for the Covered Bond Markets

Dr. Markus Herrmann

LBBW

08.2020

Since 2013, when IOSCO (The Board of the International Organization of Securities Commissions) published their “Principles for Financial Benchmarks” and 2014, when the FSB (Financial Stability Board) published its report “Reforming major interest rate benchmarks”, several years passed with countless working group meetings, numerous recommendations, regulatory statements and public consultations by the various supervisory bodies.

It is now the year 2020 that brings to the markets the first real life transformation of the old “IBOR” world into the new regime of (nearly) risk-free rates (RFR).

Manipulations of reference interest rates in the past and a significant decline in turnover in the underlying money markets have triggered a reform process that is now being implemented in all major currency areas. In Europe, this culminated in the EU Benchmarks Regulation (BMR), which came into force in 2018. The regulation became the catalyst for concrete changes in the two most important euro rates EONIA (Euro OverNight Index Average) and EURIBOR (Euro Interbank Offered Rate). Outside the EUR-context, users of LIBOR (London Interbank Offered Rate) in their respective currencies must also prepare for far-reaching changes in the coming 18 months, as LIBOR is to be phased out by the end of 2021.

This article explores the specific implications of the IBOR-Reform for the covered bond markets and will try to assess where we stand in the main issuing currencies with respect to the transformation of the existing benchmarks: from “old” EURIBOR or EUR LIBOR to “new” EURIBOR or €STR, from EONIA to €STR, from GBP Libor to SONIA, and from USD Libor to SOFR. We look at the timetables set by the respective regulators, with a main deadline being the end of 2021, and analyze the relevance of the new rules for global covered bond issuance, both already outstanding and to be issued.

Directly impacted are those covered bonds issued in a floating rate (FRN) format, so we look at the historical issuance pattern FRN vs fixed rate, and analyze the drivers for FRN issuance in the context of the rate cycle – maybe there is a renaissance ahead? Also impacted are fixed rate covered bonds with a soft bullet (SB) maturity structure, which in most cases revert to a FRN for the extension period. Other relevant aspects to be addressed are the underlying market fundamentals and collateral structures (e.g. fixed vs floating rate mortgage loans, hedging mechanisms, interest and liability swaps etc.), which all will be affected by the new benchmarks.

Among other things, market participants need to offer new products, prepare for their use and actively contribute to the creation of liquid markets. In addition, legacy contracts must be converted or redesigned and existing processes, models and IT systems must be reviewed and adapted. Moreover, covered bond issuers will need to adapt the transaction documentation for existing issues maturing after 2021, in many cases via a bondholder consent solicitation, re-structuring of Libor swaps into new benchmarks, adjustment of the underlying loan product in the cover pools to the new benchmark etc.

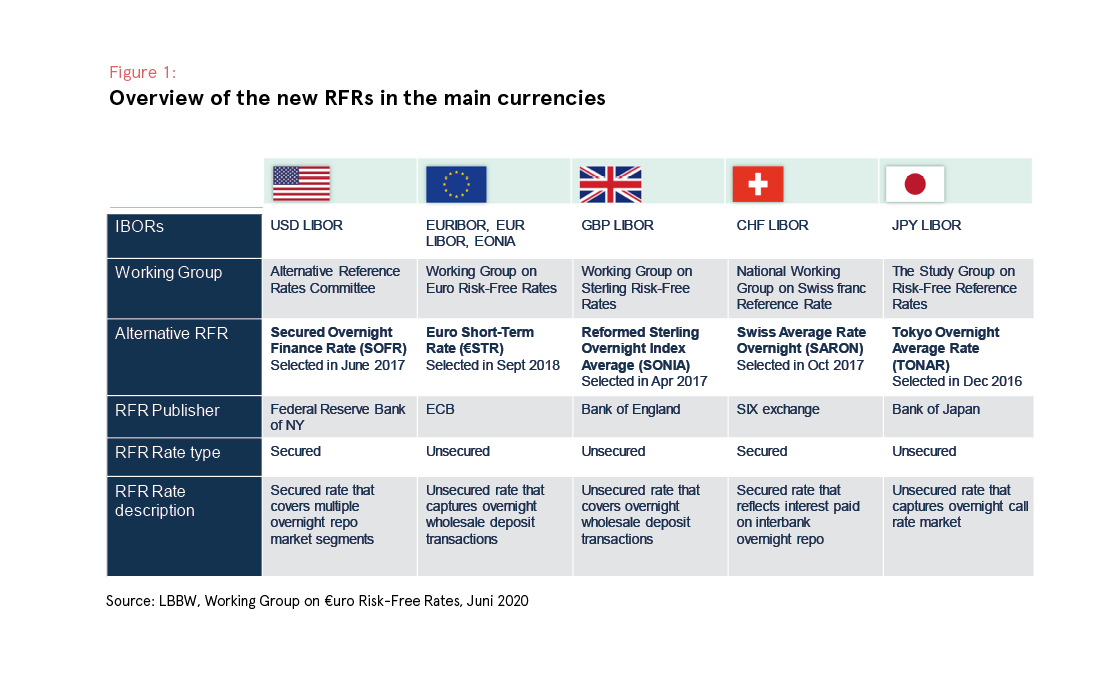

1. Overview of the new RFRs in the main currencies

The table in Figure 1 gives an overview of the new or “alternative” RFRs in the global five main currencies USD, EUR, GBP, CHF and JPY. While also other currencies have recently become increasingly relevant for the issuance of covered bonds, we note that currencies outside the EEA and Switzerland account for less than eight percent of total issuance to-date (Source: ECBC Global Issues Working Group April 2020).

Each of the alternative RFRs is published by the respective central bank, with Switzerland being the exception where the stock exchange publishes the rate. As the RFRs need to ground on robust observable overnight transaction data, to which the central banks have direct access, this seems to be the natural choice. Whereas the old IBORs had incorporated a degree of credit risk based on the average of the included panel banks, also depending on the term up to 12 months, the new overnight RFRs are supposed to be nearly risk free. The EUR, GBP and JPY RFRs reflect unsecured overnight transactions; their USD and CHF peers reflect secured overnight repo transactions. We will highlight the status quo and transition progress in more detail for the USD, EUR and GBP markets below.

2. Relevance of IBOR – RFRs for the CB market: FRN issuance

We see the direct relevance coming from the coupon format of the issued bonds, fixed or floating. Floating rate CBs to-date were typically referenced to LIBOR / EURIBOR and thus need to be transformed to a new benchmark. With an outstanding volume of EUR 567 billion (as of 12/2019, Source: ECBC Fact Book 2020 Database-), the share of FRN bonds in the global CB market is estimated to be 21%. Given the global interest rate cycle there was a trend towards more FRN issuance in recent years in many jurisdictions and the share of FRN CBs issued in 2018 rose to nearly 30% (EUR 144 billion). In 2019, the share of FRN CBs was 22% (EUR 118 billion). HoweverFRN issuance varies greatly by country.

The highest proportion of CB floaters has Italy, where they indeed outnumber the fixed rate bonds by a large margin (3x in terms of issuance, 1,7x in terms of outstanding as of 12/2019). Other Euro-jurisdictions with a high share of floaters are Spain, Austria, Portugal, Ireland and Greece; outside the Eurozone UK, Denmark and Norway stand out with a high share of floaters. This often correlates with the structure of the underlying mortgage markets, i.e. a large portion of variable rate mortgages. For these, the new benchmarks are also of immediate relevancy, both for existing loans maturing after 2021 and of course new loans that are originated during the current transition period.

We note that for some of the above-mentioned countries, particularly the southern Europeans, the majority of the issued covered bonds in recent years were retained by banks and used in interbank repo transactions and in transactions with the Eurosystem. The bonds placed in the market with investors to-date are mostly issued with a fixed rate, to conform to the preferences of what we think is the typical covered bond investor.

In contrast, France, Germany and The Netherlands, being among the top five covered bond markets, are all dominated by fixed rate issuance (floaters accounting for less than 10%) and thus will be much less affected by the transformation issues. Here fixed rate product also largely dominates the underlying mortgage markets to-date.

Soft bullet maturity structures

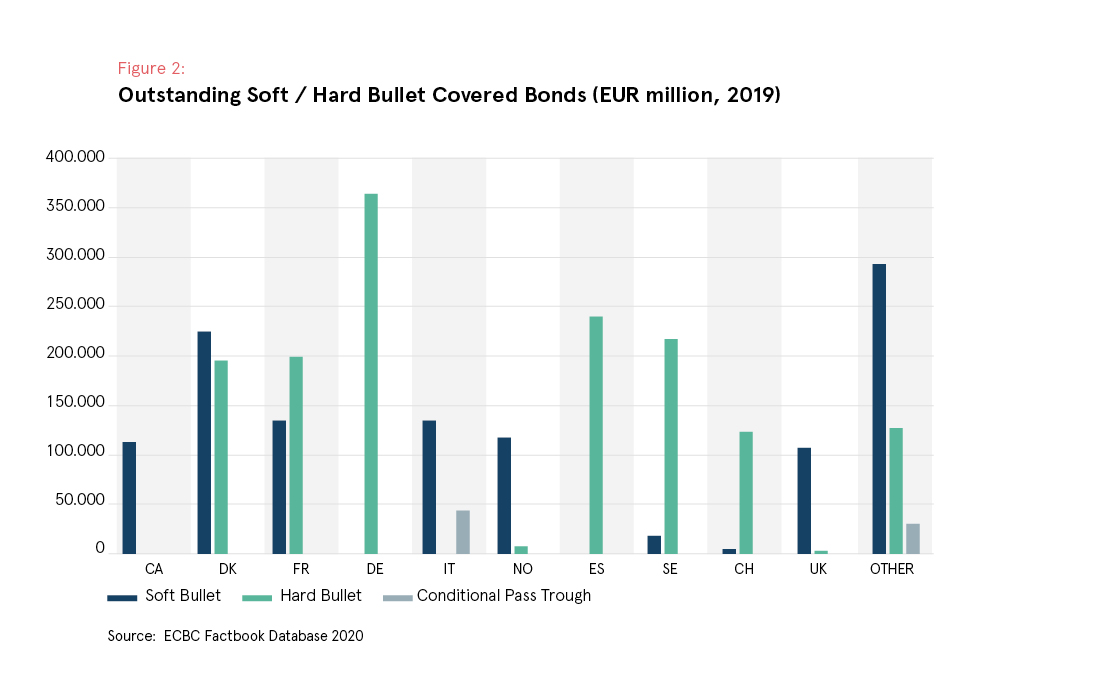

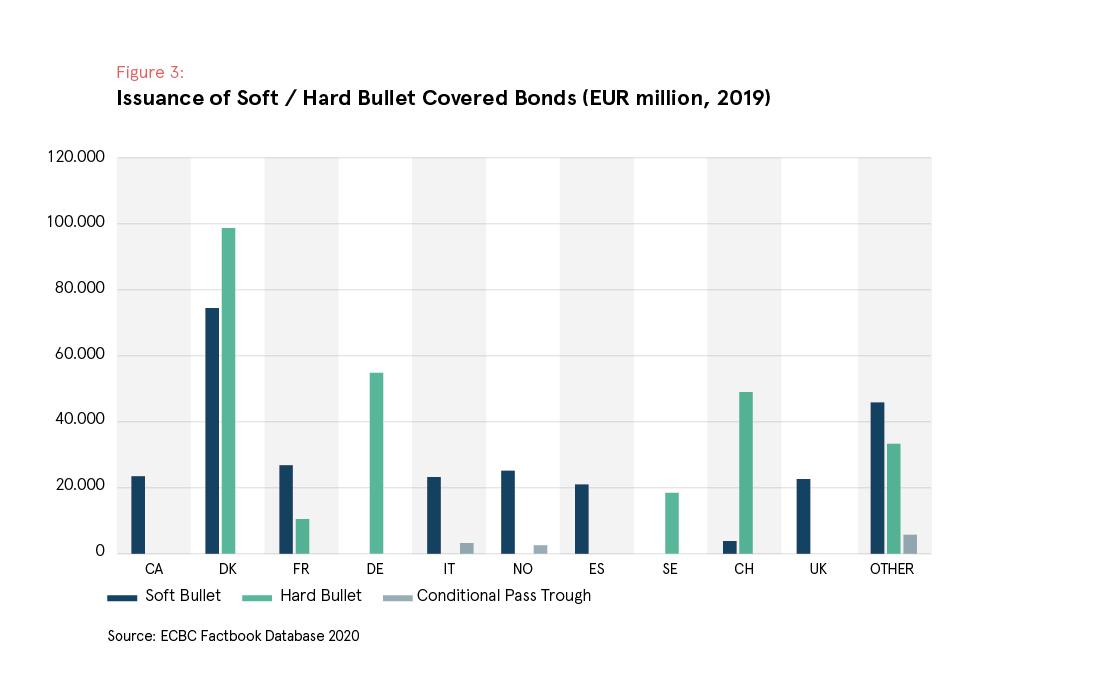

In recent years, extendable maturity structures have become a quasi-standard in the CB universe. Typically, the format of extension is a soft bullet (SB) structure, by which the regular maturity date can extend by 12 months (See Key Article in ECBC Fact Book 2019 for more detail). During the extension period, any fixed coupon in most cases reverts to a floating rate coupon with a pre-determined spread. As such, the floater element and benchmark transition comes into play even in bonds issued with a fixed coupon. While the share of outstanding SBs is currently around 40%, the share in new issues has grown recently to about 55%, SBs have been the majority of global CB issuance since 2015.

In fact, there are only a few jurisdictions, where hard bullet (HB) maturities prevail as the dominant or exclusive format: namely Germany, Spain and Sweden. Also in Denmark, a significant share of issuance is still in HB format.

For all SB structures outstanding with maturities beyond the phasing out deadlines of the old LIBORs, we believe the same transition issues need to be considered as for those bonds that were issued as a FRN from the outset.

3. EUR LIBOR, EURIBOR / EONIA to €STR: transition,status quo and progress

The new and reformed EURIBOR

The European Money Markets Institute (EMMI) – in its capacity as the administrator of EURIBOR – started the process of reforming the expert- judgement- based EURIBOR early on. In particular, the calculation methodology was to be changed to one that is underpinned to the greatest extent possible with transaction data. In the end, EMMI developed a hybrid methodology which consists of a three-level waterfall prioritizing the use of real transactions whenever available and appropriate, and relying on other related market pricing sources when necessary and thus draws on expert judgement in the absence of sufficient transactions.

The reformed EURIBOR reflects borrowing activity in the unsecured money market (i.e. not only the interbank market but now also transactions with financial counterparties outside the banking sector and with general government), while the calculation continues to be based on the voluntary contributions from a panel of banks. EMMI completed the phase-in of EURIBOR’s new methodology in November 2019. Against this background, EMMI had already received authorization from the FSMA as the administrator of EURIBOR in July 2019, in application of the BMR.

Hence, EURIBOR is considered a BMR compliant RFR and can continue to be used for existing and new contracts/instruments until further notice. In contrast, users of EUR LIBOR need to prepare for the discontinuation of rates after the end of 2021.

While the EUR FRN CB market has an outstanding volume of about EUR 380 billion (source: Bloomberg, as of June 2020), an estimated more than EUR 1 trillion (source: Bundesbank Monthly Report March 2020) of floating rate retail mortgage loans are currently outstanding, mainly in Spain and Italy. Most of them are referenced against EURIBOR, and against this backdrop, the effort to reform the existing benchmark seems very worthwhile, as it saves the market participants from the need to migrate millions of retail mortgage contracts to a new benchmark.

Fallback solutions are needed nevertheless

Even though the reformed “new” EURIBOR can continue to be used as a reference interest rate beyond 2021, market participants should be prepared for all situations, including the cessation of EURIBOR due to a lack of panel banks or liquidity. EURIBOR’s long-term viability will depend crucially on the administrator and the willingness of the panel banks to continue contributing to the calculation as well as on the liquidity of the underlying market going forward.

As the Bundesbank recently observed (Monthly Report 03/20), manipulations, the more stringent international requirements for contributors to benchmarks and the associated legal risks have significantly dampened banks’ willingness to contribute to the production of reference rates in recent years. Accordingly, 26 banks have left the EURIBOR panel since 2012, taking the current total to 18. These currently include

- Banks from EU countries participating in the Euro: Belgium, France, Germany, Italy, Luxembourg, Netherlands, Portugal, Spain;

- Banks from EU countries not participating in the Euro: UK;

- while the international non-EU banks (but with important Euro zone operations) are among the 26 banks that have left the panel.

Over the same period, membership of the EONIA panel fell by 15 to 28 banks at last count. This is also a reflection of the overall reduced market liquidity, as unsecured trading activity between banks (interbank trading) has decreased considerably in past years.

In order to fulfil the IOSCO Principles and the requirements of the BMR, contracts must contain provisions for the event that the benchmark used ceases to be provided. Therefore, robust fallback solutions should be integrated into existing contracts where possible.

While market participants await recommendations for specific fallback provisions, a generic

fallback provision, as per below, may be considered for inclusion in contracts:

€STR as recommended fallback solution by Working Group on €uro Risk Free Rates

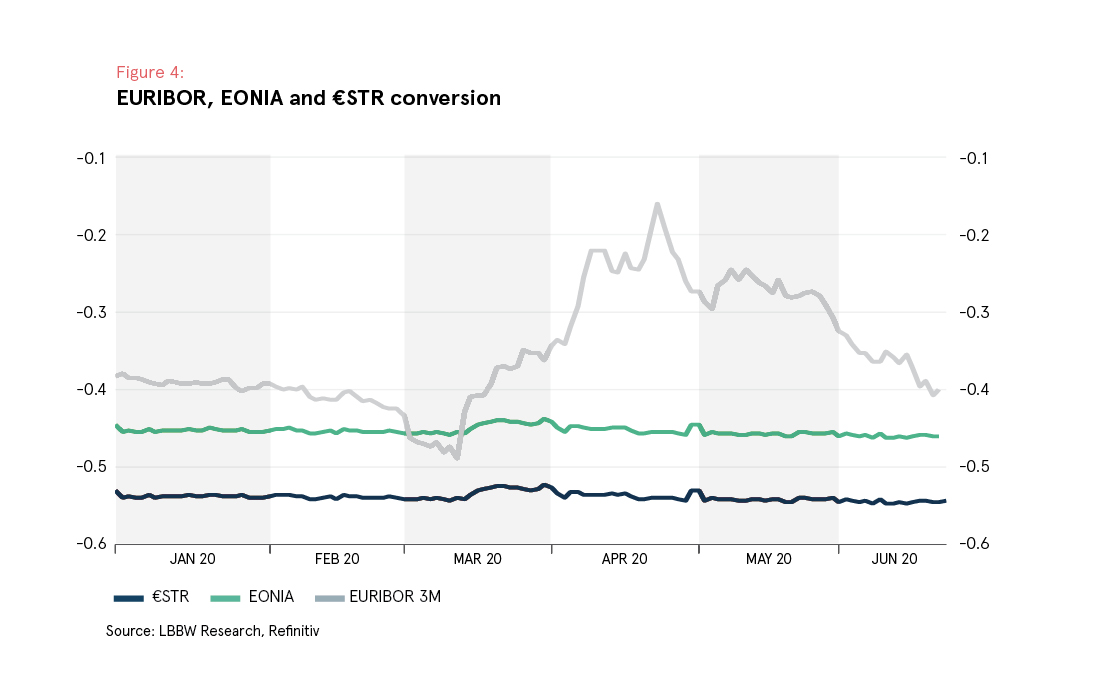

For the euro area, the introduction of the €STR marks the first big step in the path of reform towards using robust risk-free reference rates. It is now in the hands of market participants across the board to actively pursue the use of the €STR and establish liquid, €STR-based markets. At the same time, workable €STR-based fallback provisions need to be incorporated into contracts referencing EURIBOR in order to improve their robustness, as it is currently recommended by the WG on €uro Risk Free Rates. In future, market participants could likewise consider using the €STR or €STR-based term rates as a direct alternative to EURIBOR for certain instruments or contracts.

However, the euro area working group’s work on €STR-based fallbacks for EURIBOR has not yet been concluded, particularly the transformation of the overnight rate into a term rate up to 12 months as we have with EURIBOR is still under discussion. Several approaches can be employed, in analogy to the other RFRs, using either a backward-looking or forward-looking calculation method (the latter is the case for the IBORs incl. EURIBOR).

This, among other things, contributes to the fact in our view, that to-date, only a handful of issuers including the German agencies LBANK, EIB, KfW, as well as French BCFM have piloted EMTN issues referenced against €STR so far for a total outstanding volume of a mere EUR 3,9 billion (Source: Bloomberg, June 2020).

EONIA transition to €STR

EONIA does not meet the regulatory criteria required to comply with European Benchmark Regulation and will be published for the last time on 31st December 2021. Since 2 October 2019, EONIA has been published daily on the basis of a reformed determination methodology, which is €STR + 8.5 bps. EMMI will continue to publish EONIA every TARGET day until 3 January 2022, the date on which EONIA will be discontinued.

EONIA is not typically referenced in bonds, but there was some limited usage of EONIA in the European repo market. Firms must prepare for EONIA’s cessation at end-2021 in order to avoid legal uncertainty regarding the terms of their transactions once EONIA ceases to be published.

Thus, market participants with outstanding EONIA-linked transactions need to amend their legacy EONIA transactions, either to include industry-standard fallbacks or amend the reference rate from EONIA to €STR (and agree on a compensation exchange with their counterpart) or €STR + 8.5bps.

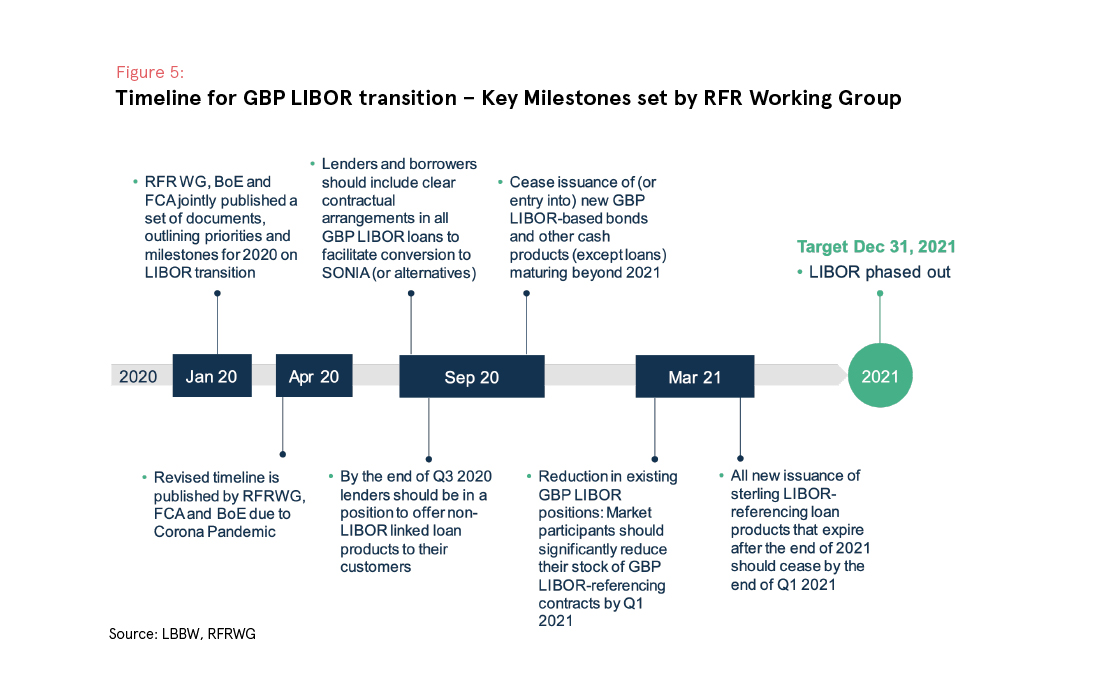

4. GBP LIBOR transition to SONIA: status quo and progress

The UK’s Financial Conduct Authority (FCA) and the Bank of England (BoE) are pushing hard for the institutions they regulate to replace LIBOR with new reference interest rates – particularly SONIA – by the end of 2021. Within sterling cash markets, transition to SONIA in the bond market has been largely completed. In this respect, the UK market is well ahead of its peers, helped by the fact that SONIA is a long-established (reformed) RFR. In the loan markets, including mortgage loans, lenders are asked to continue to work in order to make SONIA-based products available before the end of Q3 2020 and some borrowers will be ready to take advantage of these alternative products before then. Market makers were expected to change the market convention for GBP interest rate swaps from LIBOR to SONIA by the end of the second quarter. The market-led Working Group on Sterling Risk-Free Reference Rates (RFRWG) has made it a priority to stop issuing LIBOR-based cash products by the end of Q3 2020, which the regulators applaud.

The Bank of England penalizes Libor-linked cash products maturing after 2021 in its liquidity injection operations, with additional haircuts to come into effect after 3Q20, and they will increase progressively.

The LIBOR transition particularly affects UK covered bonds issued as floaters (as well as the investors holding the bonds). The percentage of floating-rate covered bonds has increased considerably in recent years. Ten years ago, floaters made up only 10% of new issues. In the years since 2017, they have accounted for roughly 2/3 of issuance (cf. Figure 3). Floaters now make up 34% of the total outstanding value of UK covered bonds.

Issuance of new SONIA-linked covered bonds

As of June 2020 we count an aggregate of GBP 57 billion worth of SONIA-referenced FRN bonds issued in the UK market, of which more than half, GBP 30 billion, are covered bonds (Source: Bloomberg). The last GBP LIBOR-referencing UK covered bonds were issued in April 2018; since then, institutions have only been issuing SONIA floaters. In contrast, nearly all the fixed-rate issues have been denominated in foreign currencies, particularly in EUR (84% cumulatively over the years). The upcoming benchmark transitions for other currencies (such as EURIBOR “new” and €STR in EUR, SOFR in USD) also affect the UK covered bond market since the soft bullet structures for the potential extension periods use a floating rate coupon whose benchmark will also have to be changed.

Another highly important aspect in the transition process is the use of asset swaps to hedge the interest rate risks in the UK cover pool assets versus the funding instruments, i.e. the covered bonds. In the past, the asset swaps would be concluded on the basis of LIBOR and would constitute an integral part of the respective covered bond issuer’s funding structure. Since the new FRNs issued since 2018 reference SONIA, the asset swaps will also have to be restructured in order to avoid a mismatch of the referenced benchmarks.

Transition of legacy transactions

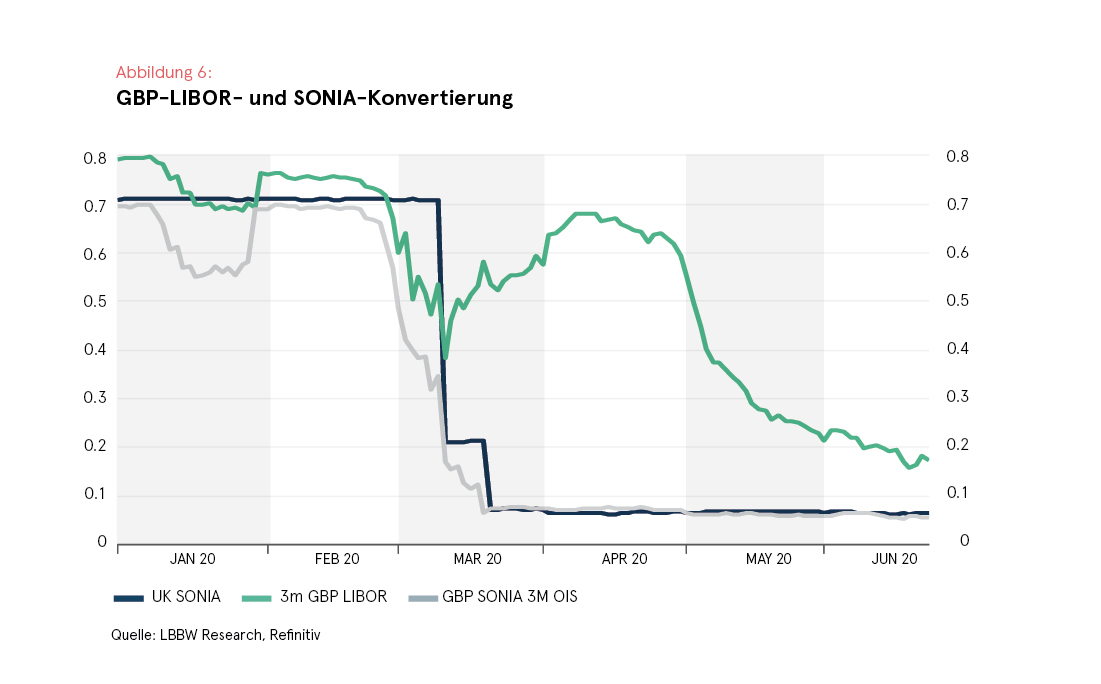

The industry-led RFRWG has made progress on its implementation plan in the past two years, but many details with respect to the transition of legacy transactions (bonds, loans etc.) are only being tested now. The new reference rate that replaces LIBOR is based on the SONIA Overnight Index Swap rate (SONIA OIS). Transitioning to the new interest rate will require fair spread adjustments for each legacy LIBOR contract in order to prevent the transfer of economic value between the parties (and thereby creating winners and losers). Irrespective of the new interest rate, a spread adjustment will require a permanent change to the contracts. How this plays out in practice is being tested as the issuers are initiating their transitions one-step at a time. The transitions completed thus far have been based on the interpolated maturity-adjusted basis between the original LIBOR benchmark (e.g. 3M GBP LIBOR) and the daily SONIA rates compounded over the same period (e.g. 3 months) in arrears.

It is our understanding that, among UK covered bond issuers, most have already successfully executed solicitations for bondholder consent to the bondholders for their covered bonds being affected. Since the change is being made in response to political/regulatory requirements, bondholders have been asked to grant their consent without receiving a consent fee, especially because the ultimate goal is to organize the transition to have the smallest possible impact on the market values of the bonds.

Rating agency assessment of UK CB transition to SONIA

In an April 2019 article, Moody’s welcomes the growth in issuance of GBP SONIA covered bonds for various reasons and labels the trend as broadly credit positive (Covered bonds – UK: Robust demand for Sonia issuance is credit positive, 24 April 2019, Moody’s). The agency believes the risk of currency mismatches has been reduced, particularly as Brexit unfolds, since the funding is denominated in local currency and strengthened by the domestic investor base. Foreign holders of UK covered bonds may be at more or less of a disadvantage, depending on the underlying exit scenario, which in turn could result in higher funding costs for UK mortgage lenders.

Moody’s highlights the interest rate mismatches between variable-rate cover pool assets and the fixed-rate covered bonds mentioned above. This risk is normally hedged by interest rate swaps, but we believe a matched funding profile would be more effective and affordable and thus render issuers less sensitive to changes in interest rates.

Standard & Poor’s expects the switch to the new benchmark will be kept largely value-neutral by the underlying mechanism and so will be credit neutral for bondholders in economic terms. However, S&P is unwilling to rule out rating impacts from the operational challenges of switching the various bonds, cover pool assets and asset and interest rate swaps over to SONIA at the transaction level.

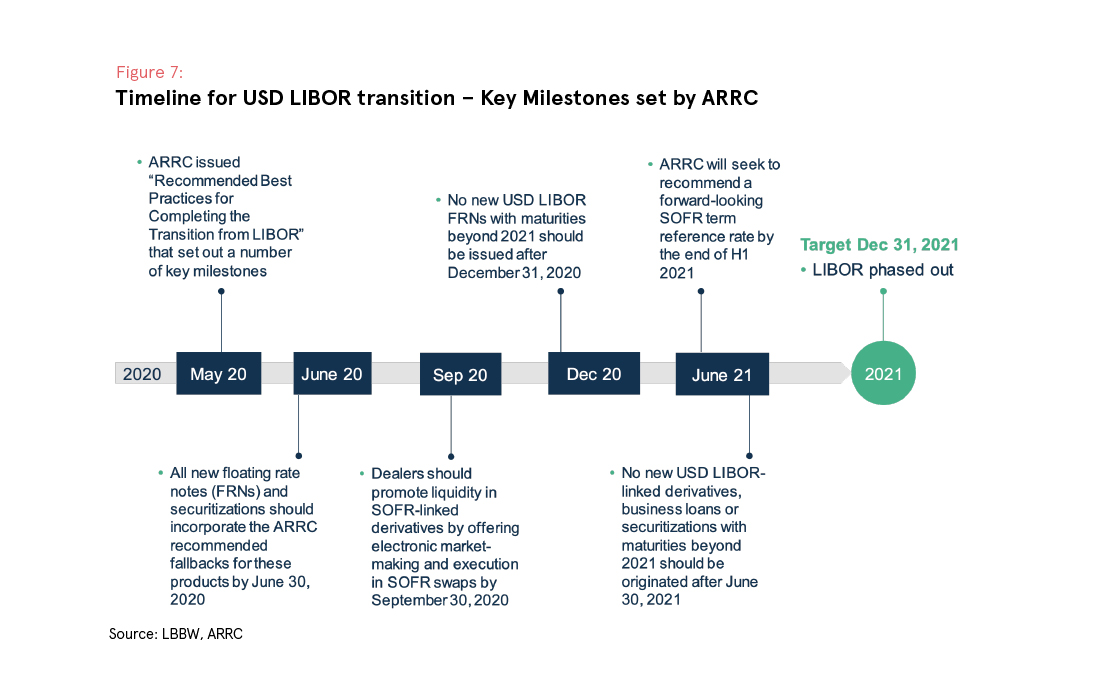

5. USD LIBOR transition to SOFR: status quo and progress

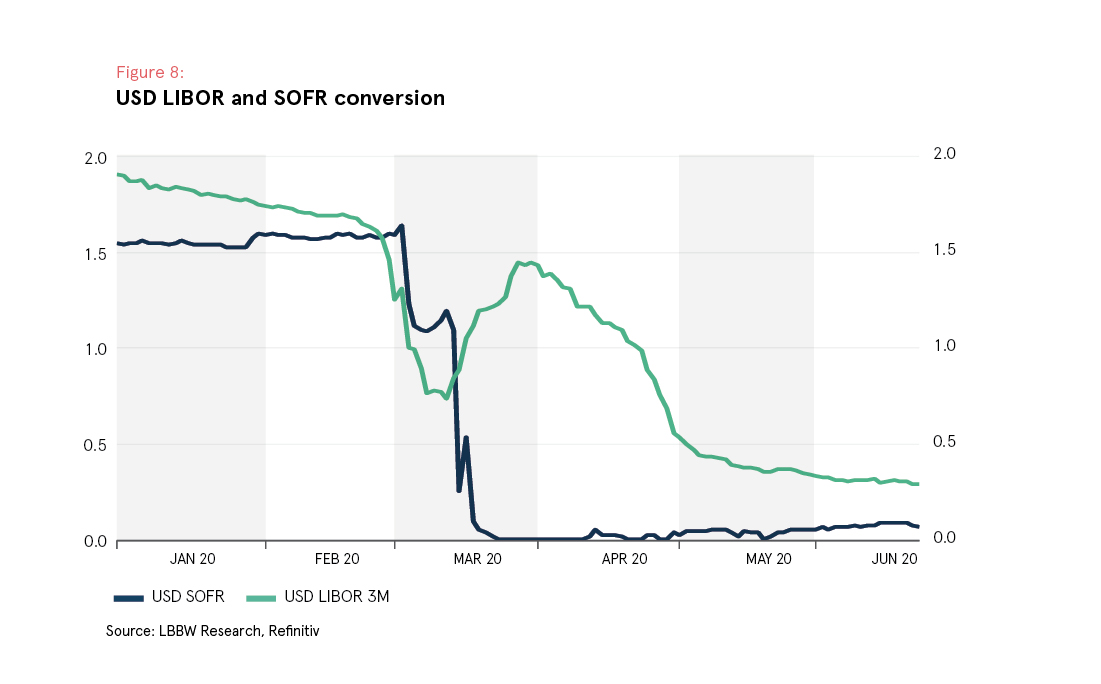

In the U.S., the Alternative Reference Rates Committee (ARRC), a group of private sector market participants and public sector officials, was convened by the Federal Reserve Board and the New York Fed to ensure a successful transition from USD LIBOR. The ARRC selected the Secured Overnight Financing Rate (SOFR), which is a broad measure of the cost of borrowing cash overnight in the U.S. Treasury repo market, as the recommended alternative RFR to USD LIBOR.

The final conventions for SOFR-based FRNs, loans and securitizations should have been established by mid-2020, and it is expected that liquidity in SOFR-based derivatives & cash products grow and, as market participants adopt the ARRC’s recommendations, expect this growth to accelerate throughout 2020 and 2021 and impact liquidity in USD LIBOR.

Transition of USD LIBOR legacy transactions

Currently USD 180 billion worth of debt referenced to SOFR is outstanding (Source: Bloomberg), mainly unsecured bank debt, with no CBs so far included. In order to assess the legacy CBs that need to be amended to the new SOFR-based reference rate, we currently count 26 USD-denominated FRN CBs. Out of these, 16 are maturing in 2022 and beyond, for a total outstanding volume of USD 7.9 bn. All of them come from European issuers, mainly Spain and Germany.

In cooperation with the Treasury Department’s Office of Financial Research, the New York Fed is now publishing three daily compounded averages of SOFR in arrears: “30-day Average SOFR”, “90-day Average SOFR”, and “180-day Average SOFR”, in addition to a daily index that allows for the calculation of compounded average rates over custom time periods: the “SOFR Index”.

Summary and Outlook

In the three main currency areas, we see a very different speed and momentum concerning the transition to the new RFRs. The UK market seems to be leading ahead, with new issuance of FRN bonds referenced against SONIA and legacy bonds being migrated by amending the documentation via investor consent solicitations. This process was clearly helped by incentives given by the BoE, namely to increase the haircuts of bonds still referencing the old LIBOR. At the other end of the progress spectrum seems to be the EUR market, where a large retail market linked to EURIBOR made it difficult appearently to migrate to €STR with the same rigor as in the UK. Thus, the reformed EURIBOR can remain in play for the foreseeable future, as long as panel banks and market participants support it with quotes and liquidity. €STR meanwhile is being developed as a fall back solution. The USD market finally stands in the middle, with SOFR being widely adopted as the new overnight benchmark for new short term unsecured bank funding.

For covered bonds, the final say about which approach towards a RFR-term rate is adopted will be one of the decisive factors determining the speed of transition. Overall, the global CB markets will increasingly need to look at the technical and legal issues of IBOR transition in the coming 18 months, as per December 2021 most of the existing IBOR benchmarks will be phased out and legacy bonds and loans need to be migrated to new RFRs by that date.