On 16 December 2021, the ECB delivered less than markets expected with respect to the size of the APP and TLTRO, while the end of PEPP net purchases in March was widely anticipated

The decision on the PEPP is not directly relevant for covered bonds, in our view, and the change in APP purchase volumes has only a tangential effect. However, the communication that TLTRO will become less generous from June 2022 is good news for covered bond supply.

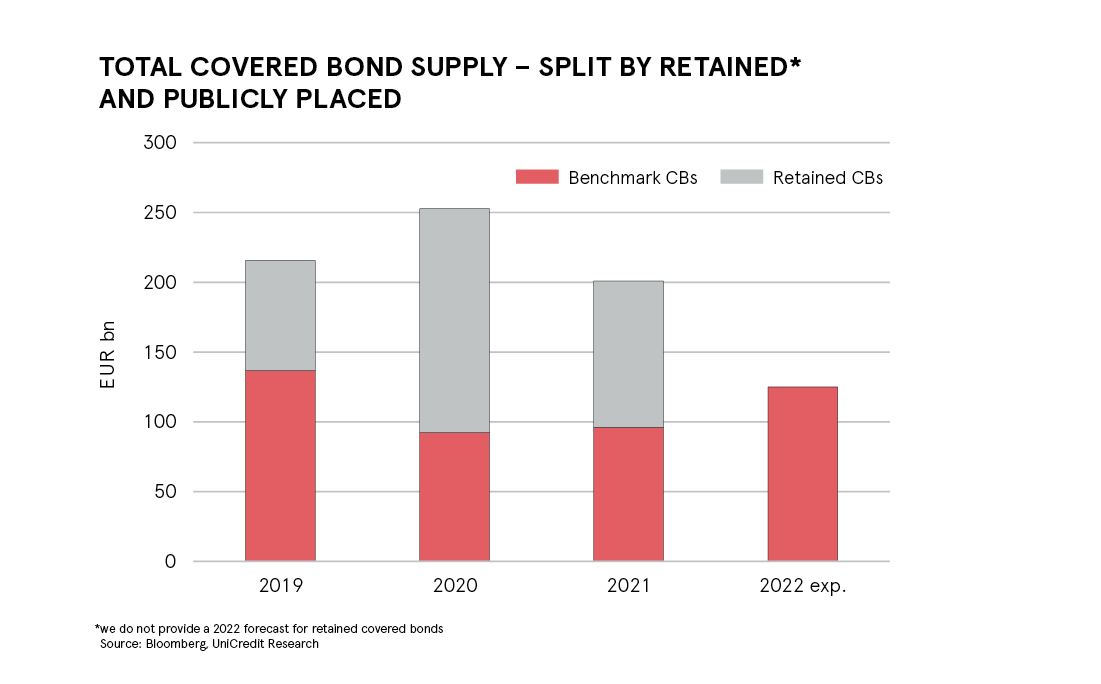

We expect banks to increasingly shift their funding from TLTRO III (including the use of retained covered bonds) to publicly placed covered bonds. This is the main reason that we expect supply volume to increase in 2022 to EUR 125bn from EUR 95bn in 2021.

Given the positive environment for covered bonds and a sufficient number of working days in the first week of the new year, we expect covered bond issuance to be lively right from the start.

Covered bond-relevant aspects of the ECB decision

On 16 December, the ECB delivered less than markets expected with respect to the size of the APP and TLTRO, while the end of PEPP net purchases in March was widely anticipated.

The end of PEPP net purchases in March 2022 was widely anticipated. Net purchases in 1Q22 will be carried out at a “lower pace” than in the previous quarter. The ECB will then discontinue PEPP net purchases in March. The reinvestment horizon for the PEPP was extended by one year to until at least the end of 2024. Flexibility in asset purchases will be retained through a “silent” PEPP.

The ECB has outlined an APP path that envisages monthly purchases of EUR 40bn in 2Q22 (the first quarter without PEPP net purchases), EUR 30bn in 3Q22, and EUR 20bn from October 2022 “for as long as necessary to reinforce the accommodative impact of the policy rate”. Ahead of the meeting, our economists had expected average monthly purchases of about EUR 40bn from April to December 2022. Therefore, the decision was a hawkish surprise.

In June, the ECB will discontinue the special (very favorable) TLTRO III conditions, but the GC will “assess the appropriate recalibration of its two-tier system”. This indicates that the ECB will scale back its highly incentivized liquidity support, reverting to the tiering multiplier as the main tool to relieve banks from the side effects of negative rates.

Impact on covered bonds in 2022

PEPP:

The decision on the PEPP is not directly relevant for covered bonds, in our view, as the amount of covered bond holdings under this program are negligible, at just EUR 6.1bn (as of November 2021) or less than 0.4 % of total PEPP holdings (EUR 1.55tn). During 2021, net purchases amounted to only EUR 3.0bn. However, an indirect impact could result from spillover effects from the SSA market. If spreads of SSA bonds widen due to reduced ECB demand for these bonds, this could exert pressure on covered bonds as well. Given that covered bonds tend to trade with a spread pick up over SSA bonds, rising SSA spreads could push covered bond spreads upwards. However, given the conditions on the PEPP termination, in combination with the APP increase, we see this risk as limited.

CBPP3:

The increase in the volume of the APP in 2022 to mitigate the end of the PEPP, will not have a significant direct effect on covered bonds. However, it will definitely continue to provide them with strong and spread-supportive demand.

Purchase volumes of the APP, including the CBPP, will increase from EUR 20bn to EUR 40bn in 2Q22, before declining to EUR 30bn in 3Q22 and to EUR 20bn from 4Q22 onwards. Therefore, demand for covered bonds can be expected to be strong. However, we do not expect the volume of net covered bond purchases in 2022 to change significantly.

In 2021, the average monthly net purchases in covered bonds under the APP/CBPP3 were around EUR 1.0bn or 5 % of the EUR 20bn overall monthly purchases. This amounts to around EUR 12bn in 2021. We assume that this EUR 1.0bn per month average will remain more or less constant and will not increase significantly in 2Q21 when APP purchases increase to EUR 40bn per month.

We see two main reasons for this: 1. the increase in the APP is due to the termination of the PEPP and mainly targets government and SSA bonds; and 2. covered bond supply is always strongest in the first quarter (close to 40 % of annual supply on average over the past ten years), when the APP will be unchanged at EUR 20bn per month, and tends to decline in the second quarter (to 23 % of annual supply on average) when the volume of the APP jumps to EUR 40bn per month. Thus, we assume that the absolute amount of EUR 1.0bn will remain broadly constant throughout 2022 rather than the 5 % share of covered bonds under the APP. However, even if the 5 % share did remain constant throughout 2022, this would lead to net purchases of EUR 16.5bn, not significantly higher than the EUR 12.0bn we assume.

In addition, around EUR 40bn of covered bonds in the ECB portfolio will mature in 2022, and they are likely to be reinvested. This could lead to up to EUR 52bn of total gross covered bond purchases by the ECB in 2022. Given that around two thirds, or EUR 80bn, of our 2022 supply forecast of EUR 125bn comes from eurozone banks and is thus eligible for purchase, this will provide a highly stabilizing factor for covered bond spreads next year, despite the active issuance expected. It will also reduce execution risk, especially in longer-dated covered bonds.

TLTRO III:

On Thursday, the ECB decided not to extend the favorable -100bp TLTRO III borrowing rate beyond June 2022 and it did not give any indication about a follow-up TLTRO program. The key sentence of the ECB statement from a covered bond perspective was, in our view, “As announced, we expect the special conditions applicable under TLTRO III to end in June next year.” It is our understanding that the previous highly attractive TLTRO rate of -100bp will be reset to the deposit facility rate of -50bp, at best.

This is clearly positive for covered bond supply in 2022. We expect banks to increasingly shift their funding from TLTRO III (including the use of retained covered bonds) to publicly placed covered bonds. This is the main reason that we assume supply volume will increase in 2022 to EUR 125bn from EUR 95bn in 2021.

Publicly placed covered bonds to regain dominance over retained bonds

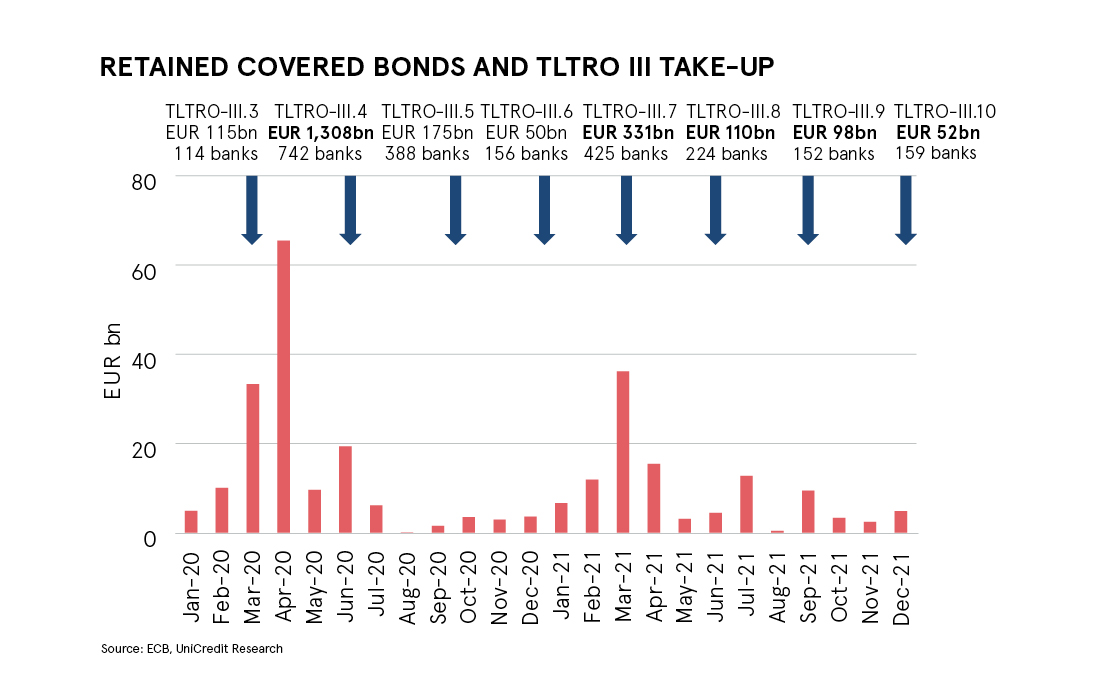

Retained covered bonds offer a benefit to issuers in that they can be used flexibly as collateral. Once on hand, issuers can decide if and when to use them as collateral for repo purposes and when to take them back for whatever reason. Thus, the amount of retained covered bonds issued closely correlates with the amount banks took up under TLTRO-III.

EUR 270bn of retained covered bonds were issued between January 2020 and December 2021, EUR 160bn in 2020 and EUR 110bn in 2021. These amounts compare to publicly placed covered bonds of EUR 92bn in 2020 and EUR 95bn in 2021. Thus, the total amount of covered bonds issued in 2021 was EUR 205bn, 54 % of which were retained and 46 % placed with investors. As retained covered bonds can be relatively easily transformed by the issuer into covered bonds used for public placement, there is significant potential for issuance in 2022 and beyond.

While the large issuance of retained covered bonds was at the expense of publicly placed covered bonds in 2021, on the positive side it shows that there is sufficient eligible collateral available for the issuance of covered bonds going forward.

We expect the scheduled end of the extremely favorable TLTRO conditions in June 2022, and indications that banks will make less use of ECB funding tools, to have a positive effect on covered bonds as retained covered bonds are gradually transformed into publicly placed covered bonds. Thus, a key driver for lower covered bond supply volumes in 2021 will become less important next year. This is reflected in our 2022 supply forecast, which envisages the volume of publicly placed covered bonds (our forecast: EUR 125bn) exceeding the amount of retained covered bonds issued.

Lively issuance can be expected in January

Given the positive environment for covered bonds and a sufficient number of working days in the first week of the new year, we expect covered bond issuance to be lively right from start.

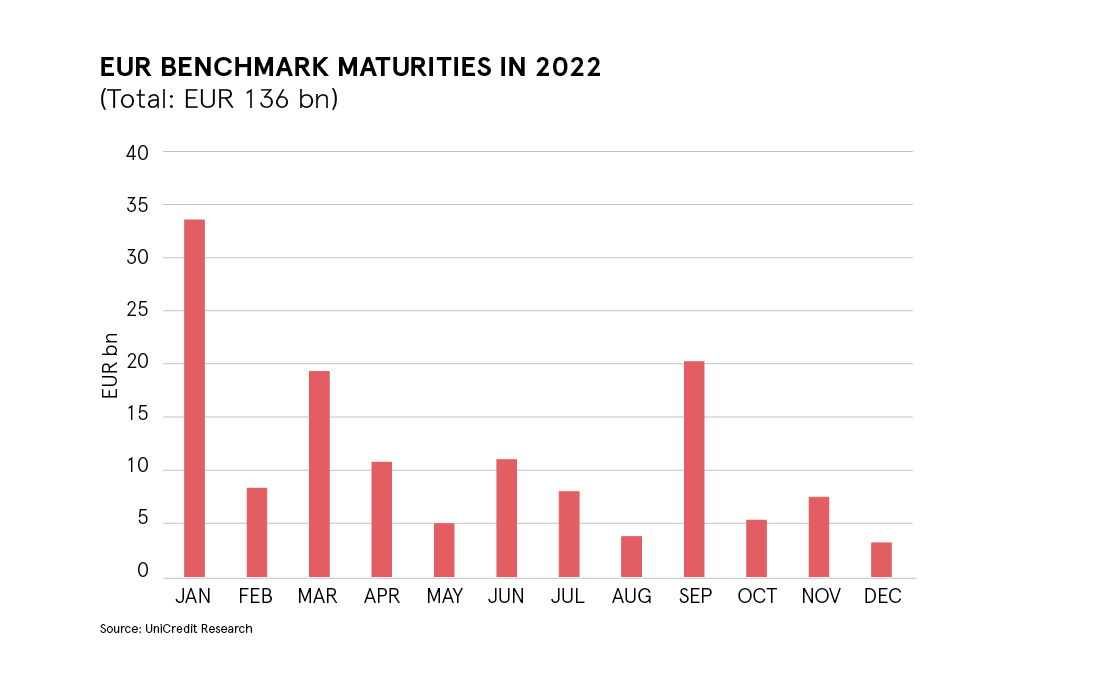

The average share of supply in January relative to the full-year supply over the past ten years is 21 %. Applying this 21 % share to our supply forecast of EUR 125bn for 2022, brings us to around EUR 27bn. This is also pretty much in line with average absolute volumes over the past ten years, which stand at EUR 25bn, and even over the past 25 years (EUR 23bn). The EUR 27bn expected in January 2022 would compare favorably to maturities of EUR 33.5bn, thus resulting in negative net supply in January. This should create a stable spread environment, despite the active issuance.