CBPP3.1 – Will the ECB buy 50 % of eligible covered bond supply?

Franz Rudolf

UniCredit Bank AG

10.2019

At the ECB meeting on 12 September, a bold package of stimulus measures was announced. Besides a deposit-rate cut, a two-tier system of reserve remuneration and an improvement of TLTRO-III, a new quantitative-easing (QE) program was announced. The asset purchases of the QE program will affect covered bonds directly and most strongly. We have thus analyzed the ECB’s restarted covered bond purchase program (CBPP3.1) and its impact.

Facts

The ECB stated that “net purchases will be restarted under the Governing Council’s asset purchase program (APP) at a monthly pace of EUR 20bn as from 1 November. The Governing Council expects them to run for as long as necessary to reinforce the accommodative impact of its policy rates, and to end shortly before it starts raising the key ECB interest rates. Reinvestments of the principal payments from maturing securities purchased under the APP will continue, in full, for an extended period of time past the date when the Governing Council starts raising the key ECB interest rates, and in any case for as long as necessary to maintain favorable liquidity conditions and an ample degree of monetary accommodation.”

What does this mean for covered bonds?

Assuming a similar composition in terms of asset classes to that of previous programs, the share of covered bonds purchased under CBPP3.1 would be around 10% (covered bond holdings of EUR 261bn versus APP holdings of EUR 2,55bn as of 1 November 2019). Thus, our calculation of covered bond purchases is as follows: APP purchases of EUR 20bn; of this, 10% will be covered bonds. This is equivalent to EUR 2bn of covered bond purchases per month. On top of this, monthly covered bond reinvestments will amount to EUR 2bn on average, brings the total amount of covered bond purchases per month to EUR 4bn. For a twelve month period, this sums up to EUR 48bn. To put this into perspective, annual gross benchmark covered bond supply is around EUR 140bn, of which roughly EUR 100bn would be eligible Eurozone covered bonds. Thus, the ECB would need to buy around 50% of new gross supply in order to meet its targeted purchasing volumes. The split of purchases in the primary and secondary markets remains to be seen, but significantly higher demand by the ECB in order books compared to previous figures has been seen since 1 November. This will, in our view, be supportive of continuously low yield and levels for covered bonds, but it also indicates low secondary market liquidity going forward.

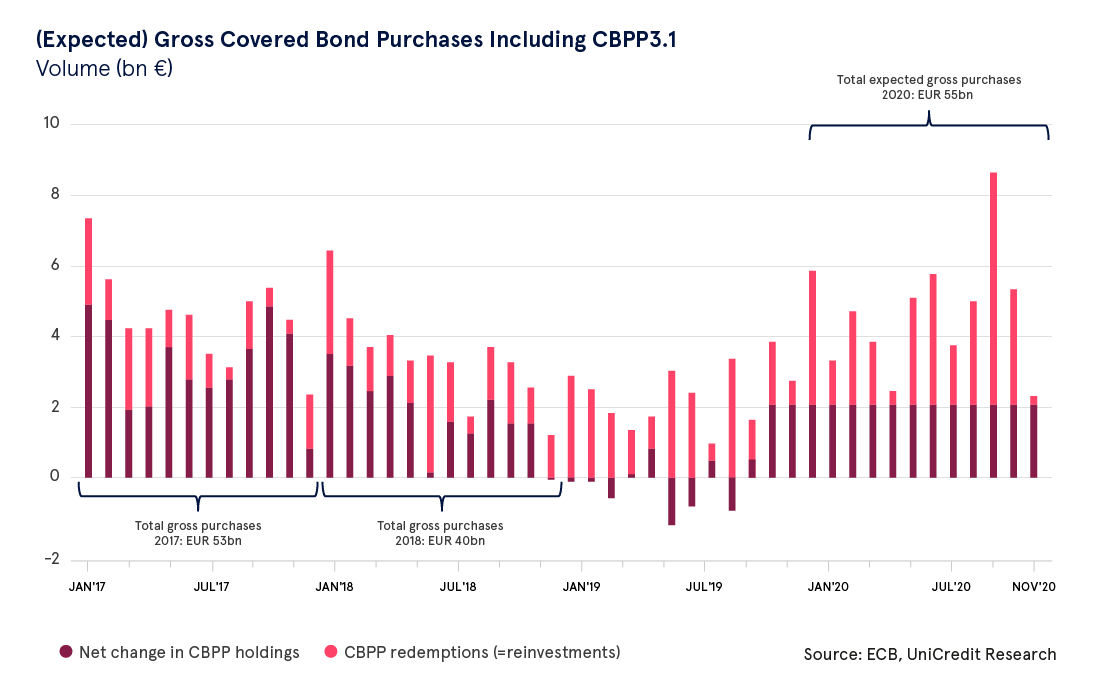

Potential gross purchases of EUR 55bn in 2020 under CBPP4

The chart shows reported net changes in covered bond holdings between January 2017 and October 2019, as well as our estimated net purchases from November 2019 onwards (dark red columns). The grey columns show reported redemptions between January 2017 and October 2020 as well as our projections for the period 2020. As mentioned above, the sum of net purchases in 2020 and the amount of covered bond redemptions reinvested amount to roughly EUR 55bn, and thus around 50% of annual eligible supply.