Covered bond supply 2021 – what will the magic number be?

Franz Rudolf

UniCredit Bank AG

Julian Kreipl

UniCredit Bank AG

01.2021

Covered bond analysts would like to look into their crystal ball to estimate the supply for next year. In the absence of such a magic tool, we looked at more than 200 issuers from 30 countries, at their redemption volumes, the impact from central-bank measures and the overall economic environment the issuing banks will be operating in. With that in mind, we made our forecast for the 2021 euro-denominated covered bond benchmark supply.

Recap of 2020

In 2020, 110 euro-denominated benchmark covered bonds have been issued by 70 issuers, with a total volume of EUR 92bn. The most active banks have been those in France (EUR 27.35bn), Germany (EUR 18.75bn) and Canada (EUR 8.75bn). The preferred tenors have been 10Y (22%), 5Y (19%) and 7Y (17%), but we have also seen tenors up to 25 years being issued. Spreads were stable at the beginning of 2020, before they experienced significant pressure during the peak of the COVID-19-induced financial-market turmoil in March and April. Spreads recovered quickly in May and June and have been grinding somewhat tighter since then. Overall, the iBoxx EUR Covered index is trading flat compared to where it was trading at the beginning of the year. For 2021, we expect covered bond spreads to be well supported due to significant negative net supply, ongoing ECB covered bond purchases and continued strong demand from investors.

Drivers in 2021

The key drivers of covered bond supply in 2021 will be the further development of the COVID-19 pandemic and the measures taken by central banks to counteract negative economic consequences. The ongoing third covered bond purchase program (CBPP3) of the ECB and, even more strongly, the impact from TLTRO III on covered bond supply will be the key drivers. We regard the implementation of the Covered Bond Directive (harmonization) as a driver of only minor importance for the supply volume but as relevant to the overall covered bond market.

Cover pool quality.

We see only a limited negative impact on cover pools resulting from the COVID-19 pandemic due to

- the dynamic nature of cover pools,

- sufficient measures to buffer potential risk, e.g. low LTVs, OC, liquidity buffers, etc.,

- the high quality of residential mortgages as well as the limited amount and diversified risk profile of commercial mortgages,

- the sound credit quality of the issuing banks and

- the supporting measures from the fiscal, regulatory and monetary policy side.

Retained covered bonds.

An important consequence for covered bonds resulting from the highly attractive TLTRO conditions in 2020 was a shift from publicly placed covered bonds towards retained covered bonds. Banks decided to issue large amounts of retained covered bonds (or own-use covered bonds) in order to place them as collateral for refinancing operations rather than publicly sell them to investors. Thus, the volume of retained covered bonds has increased significantly in 2020 with a volume of around EUR 160bn.

Due to the highly attractive conditions of the TLTRO III also in 2021, we expect retained covered bonds to remain a key topic for the sector. However, as only a small part of the retained covered bonds issued in 2020 show a tenor of one year or shorter, we do not expect that a large amount of additional retained covered bonds will be issued in 2021 and expect already existing retained covered bonds to be used for future transactions. This is also a matter of sufficient collateral available for cover pools. Thus, the amount of outstanding retained covered bonds will remain high and collateral is not expected to be freed up in the short term for the issuance of publicly placed covered bonds. However, the supply of retained covered bonds in 2021 will, in our view, be more moderate and will not be as high as in 2020.

TLTRO III and CBPP3.

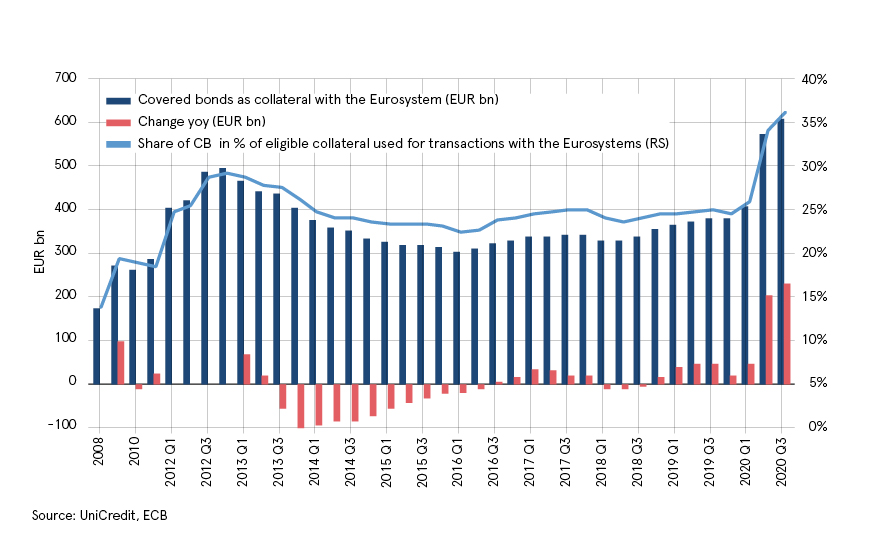

As of the end of 3Q20, the ECB reported a total of EUR 2,570bn of collateral placed with the Eurosys-tem, of which EUR 610bn were covered bonds. The EUR 610bn of collateral posted in covered bonds compare to EUR 1,673bn of eligible covered bond collateral or 36% (see chart). On top of this, EUR 288bn are held by the ECB under the CBPP3 and EUR 3.1bn under the PEPP. Thus, in total, around 54% of all eligible covered bonds are linked to the ECB, either as collateral in repo transactions or as part of the ECB’s CBPP3 portfolio. The decisions regarding TLTRO III conditions as well as the amounts purchased under the CBPP3 will be a decisive factor for covered bonds in 2021.

COVERED BONDS USED AS COLLATERAL IN EUROSYSTEM TRANSACTIONS

TLTRO III has been a key driver of covered bond supply in 2020 and will continue to strongly impact issuance in 2021. Driven by the second wave of the COVID-19 pandemic, the ECB on 10 December extended the favorable terms of TLTRO III from June 2021 to mid-2022, among others. This could mean that a large number of banks would not repay their TLTRO-III drawings early in September 2021, which would have a negative impact on the funding volume of covered bonds.

ESG covered bonds.

Since 2014, banks from France, Germany, Spain, Norway and South Korea have issued use-of-proceeds (UoP) covered bonds, which comprise green, social, sustainability and positive-impact bonds. A new record was reached in 2020 in terms of the issuance of ten UoP benchmark covered bonds, with a total volume of EUR 7.75bn (2019: EUR 6.5bn). The total volume of ESG covered bonds issued in benchmark size amounts to EUR 23.25bn.

In 2020, no new countries were added to the list of active issuers, but Sparebanken Vest Boligkreditt (green), Kookmin Bank (sustainability) and BPCE (green) are three new issuers. Furthermore, existing issuers have extended their ESG curves. French issuers have placed the most ESG covered bonds in 2020 (EUR 3.25bn), followed by Korean issuers (EUR 2bn). For 2021, we expect the ESG covered bond market to steadily expand, but due to the overall-subdued issuance forecast, it is unlikely that any new records will be set in 2021. Aside from existing issuers and countries, we think the first issuers from Finland and Austria might enter the segment this year.

Country-by-country forecast for 2021

For 2021, we expect banks from 23 countries to issue covered bonds with a total volume of EUR 95.0bn, while banks from seven countries will not be active (yet). According to our forecast, the three countries with the largest gross issuance volumes are Germany, France and Canada. Covered bond issuance in these three countries should not be materially affected by the aforementioned key drivers, i.e. the CBPP3, TLTRO and political risk, although TLTRO is also expected to weigh on supply from French and German banks. Thus, we expect new benchmark gross supply of EUR 24bn from French banks (compared to EUR 28.5bn in redemptions), EUR 12bn from German banks (compared to EUR 12.85bn in redemptions), and EUR 10bn from Canadian banks (compared to EUR 7.5bn in redemptions). We expect issuance from the Nordic region to remain strong and estimate EUR 13bn of gross supply in covered bonds from Denmark, Finland, Norway and Sweden. From Spain, which has the third-largest covered bond market by outstanding benchmark volume, we expect only EUR 2bn in issuance (compared to EUR 15.9bn in redemptions) and from Italy, we expect EUR 3bn of new supply (compared to EUR 5.8bn in redemptions). The low figures in Spain and Italy will be driven mainly by funding competition from TLTRO III. In the UK, issuance activity of banks in EUR will be impacted by the Brexit and decisions by banks as to whether to issue in GBP or EUR. Momentum in the Asia Pacific region is likely to continue in 2021, and we expect gross supply to total EUR 10bn (compared to EUR 8bn in redemptions) from Singapore, Korea, Japan, Australia and New Zealand.